It is that time of the year where we are busy buying gifts for friends and family. One pro-financial gift that you can give everyone along with yourself is some tax savings! Everybody hates to pay taxes and any savings that you get there is a blessing in disguise. However, taxes seem such a complex subject to tackle that nobody wants to touch it even with a 6 foot pole. I am also one of those that hate to read jargon and fine print, which is the tax code in a nutshell. However, this year I decided to take the plunge and find a few things that I can do to reduce my tax bill to be paid next year. I found that there are some things that I need to do by the year-end and some things that I still have time to do till the tax filing deadline. I would like to share what I learnt with you in case they are useful for your situation. Let us talk to the Wealth Wise Owl to learn more.

Some useful resources that I read/watched were

https://www.schwab.com/learn/story/year-end-portfolio-checkup-5-tax-smart-tips

https://turbotax.intuit.com/tax-tips/tax-planning-and-checklists/top-8-year-end-tax-tips/L5szeuFnE

Do THIS Now: Seven Year-End Tax Secrets That Could Save $$$

Do This Now To Pay Less Taxes In 2025

Please use the links below to jump to a specific section that you are interested in.

- Contributions to Employer 401k plan

- Contributions to Traditional IRA

- Contributions to Health Savings Account (HSA)

- Tax-loss harvesting in Taxable brokerage accounts

- Charitable donations

Conversations with Wealth Wise Owl

Hello my friend! How are you doing this fine morning? Looks like you have a cleaning day in today’s agenda.

Good morning! Yes, as you can see I have a lot of stuff outside and there is a lot more that still needs to come out of my home. It is my year end ritual and I am always amazed at how much I end up hoarding!

We are very similar in that regard. I would also store things in the futile hope that they would be useful sometime in the future. The result is a whole lot of things in my storage that I do not even remember why I kept them in the first place. I have my cleaning day scheduled for this weekend. Hope to donate a lot of stuff that someone else can definitely find useful.

That is such a good idea! It is a great way to be charitable and also good for the environment since it is a form of recycling. Plus, you can claim that as a tax deduction and reduce your tax bill for next year.

Really! I did not know about that. I have been donating every year but this is the first time I heard about claiming deductions for charitable donations. By the way, are there any other tips to reduce my tax bill for next year? I would hate to miss out on such cool information on saving taxes.

Of course! There are a few on top of my head which I can share but you should chat with a tax professional if you want to get more details. If you are managing a lot of assets then it is worthwhile to have a professional do your taxes since the amount you can save on taxes can justify their fees.

Definitely an option that I will consider in the future. My current assets are whatever I have in my retirement and brokerage accounts, so pretty manageable in my opinion. Do you have any advice there to save taxes?

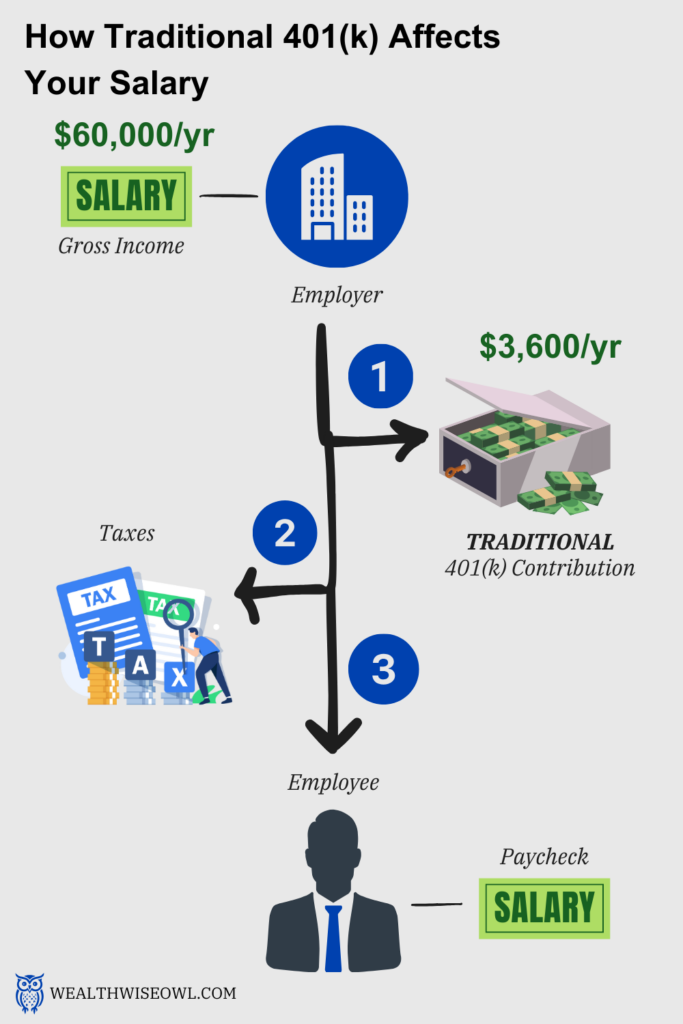

Retirement accounts are a good place to start this conversation because there are three main types that offer different tax advantages. [Check out this blog about different types of retirement accounts] The first type is the tax-deferred retirement account like the employer sponsored 401k account, 403b, 457 and traditional IRAs are some of the common ones. The contributions to this account can be deducted from your taxable income and hence offer a direct means of tax-savings. Another benefit of contributing, especially to the employer sponsored 401k plans, is the possibility of an employer match to the contributions that you make to this account.

https://www.investopedia.com/articles/taxes/11/tax-deferred-tax-exempt.asp

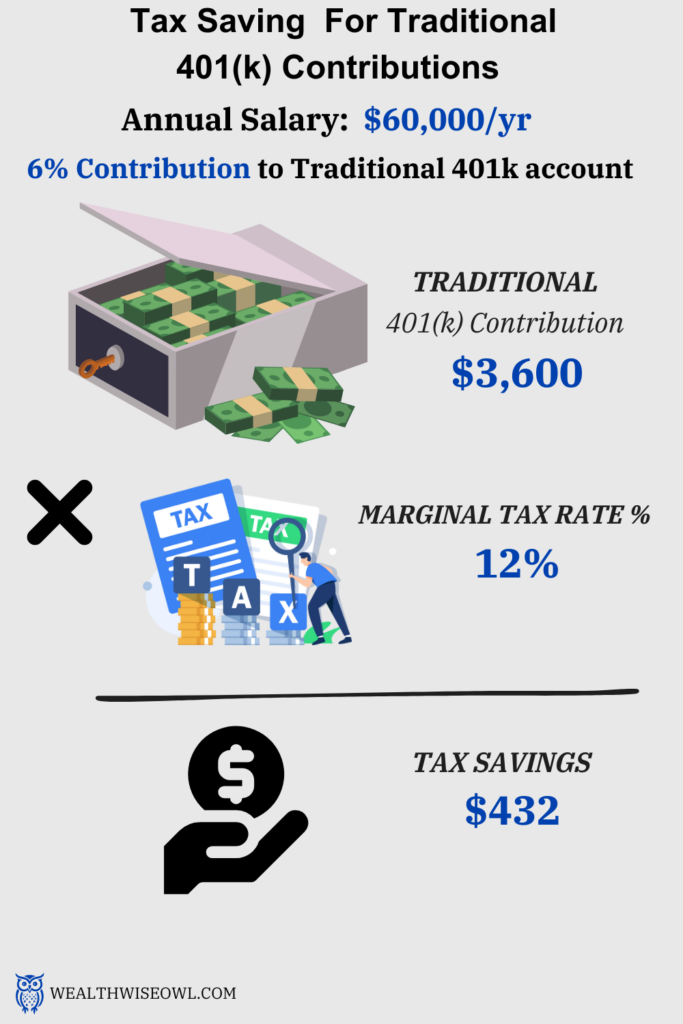

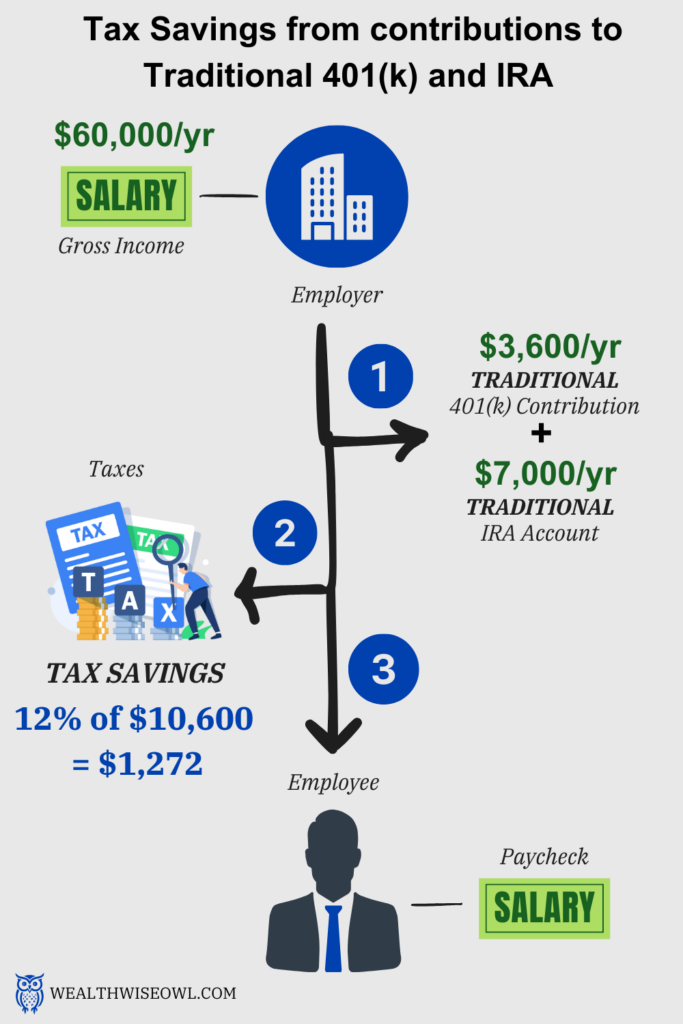

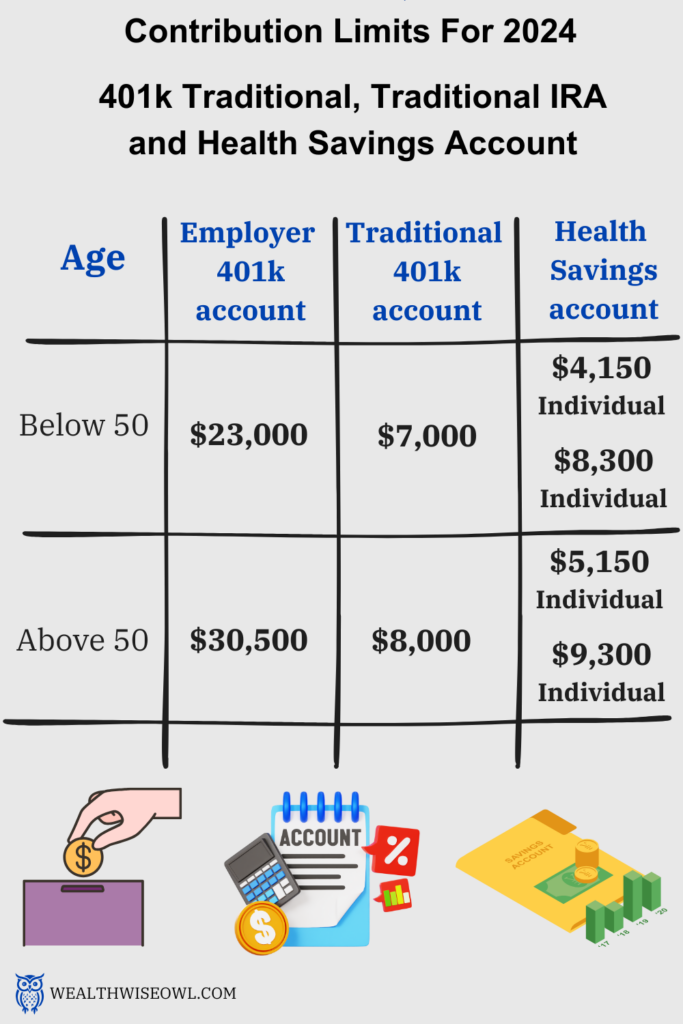

Let us take an example of an employee who earns $60,000/yr and contributes 6% of his salary to the 401k account. The employer matches 100% of the contributions up to 3% of the salary. So, the employee has contributed $3,600 (6% of salary) and the employer will contribute $1,800 (100% match up to 3% of salary). Now, the $3,600 contributed by the employee will be deducted from the gross salary i.e the taxable income will be $60,000 – $3,600 = $56,400. The contribution limit to 401k for 2024 is $23,000 for 2024 plus an additional $7,500 in “catch-up” contributions for employees who are 50 or older, so the maximum deduction is either $23,000 or $30,500 based on the employee’s age. This is a huge tax saving opportunity if you can contribute to the maximum limit.

If you need to provide a % of your salary as a contribution to 401k and want to know what percentage will get you to the maximum contribution, simply divide $23,000 by your gross salary and multiply that by 100. This will give you the percentage contribution to get to the $23,000 limit. However, if you contribute some percentage of your bonuses too to your 401k then this percentage contribution of your salary will need to be reduced accordingly.

This is great! I do have a 401k account sponsored by my employer. I will have to check if I have met my contribution limit for the year but if not I will check with my HR if they can help me figure out the percentage contribution I need to make.

Yes, it is always good to seek some help if you are not sure. Besides the employer sponsored 401k plan, another tax-deferred account that you don’t need an employer for is the traditional IRA account. You can have and contribute to both 401k and Traditional IRA accounts. The contribution limit to this account is $7,000/yr and $8,000/yr for those who are 50 years or older. Just like the contributions to 401k, these can be deducted from your salary and reduce your taxable income. So, in our example, if the employee contributes the full $7,000 towards the Traditional IRA account, then the taxable income would reduce to $49,400 (=$60,000 – $3,600 (401k contributions) – $7,000 (Traditional IRA contributions)).

Two things to remember here:

- The contributions to the traditional IRA can be made in dollar amounts at any time during the year and up to the tax-filing deadline, which is April 15 of next year.

- The contribution limit of $7,000 is for the combined contribution to Traditional and Roth IRA accounts. So, if the employee has already contributed $3,000 to the Roth IRA account then he/she can contribute up to only $4,000 to the Traditional IRA account. Contributions to the Roth IRA account will not be deducted as this is a tax-free account, where the contributions are made with after tax money and it is the withdrawal from this account that is tax-free if certain criteria are met. [For more information on tax-free accounts and criteria for tax-free withdrawals, check out this blog]

Wow! Good to know there is another option besides the employer sponsored 401k plan to increase my tax savings further. In total I can deduct up to $30,000 from my salary if I maximize contributions to both my 401k and traditional IRA account, which is amazing! One question, how do I know if it is better to contribute to the Traditional IRA account or the Roth IRA account? I understand that in the Traditional IRA account there are tax savings now but I would have to pay taxes when I withdraw the money and for a Roth IRA account it is the other way around, pay taxes now and withdraw tax-free.

You have understood the key difference of the two IRA accounts perfectly! The decision to contribute between the two boils down to the question, will you be in a higher or lower tax bracket when you withdraw the money during retirement? If you will be in a higher tax bracket than you are now then it is better to pay taxes now in the lower tax bracket and contribute more towards the Roth IRA account. However, if you are in a high income tax bracket now and will be in a lower bracket when you retire, then contributing more to a traditional IRA would make more sense. Here again, a tax professional can help since they can look at your specific situation and advice.

One thumb rule from the Money guy show is if your marginal federal plus state income tax rate is lower than 25% then contribute to a Roth IRA but this rate is 30% or higher then contribute to a Traditional IRA.

Traditional vs. Roth 401(k): Which Should You Choose for Maximum Growth?

That makes sense! I can see the logic of looking at your current and future potential tax rate to decide where to contribute. Any other accounts that I can contribute to for tax savings?

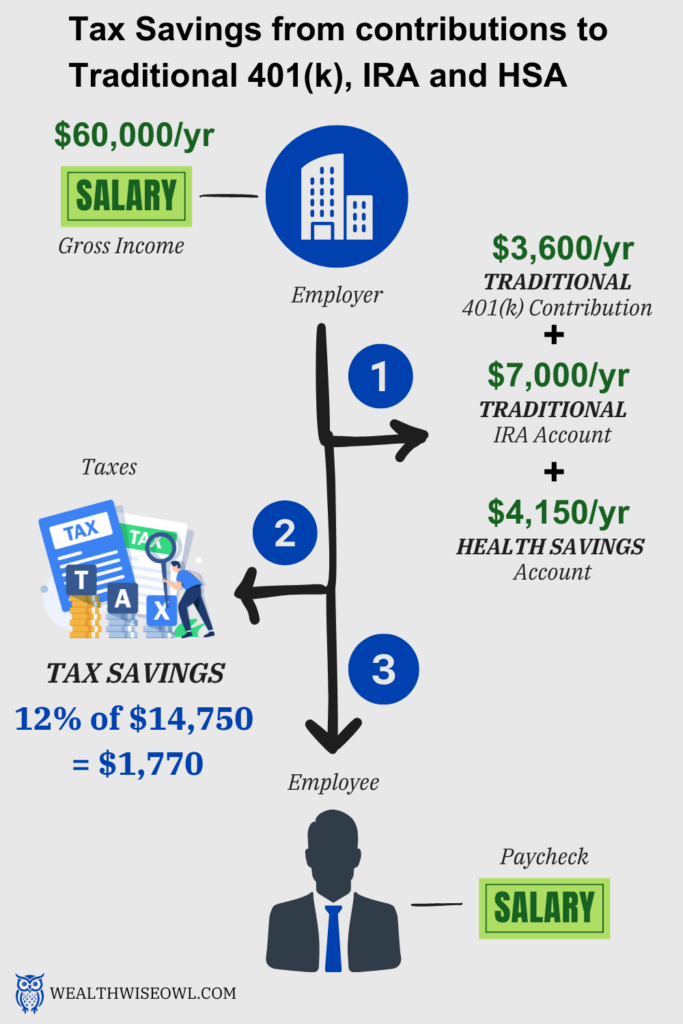

Yes, there is one more that is triple tax advantaged i.e it reduces your taxable income, the investments in the account grow tax-free and you can withdraw money tax-free for qualified expenses. This amazing account is the Health Savings account. [Check out this blog to learn more about the HSA account] You can contribute to this account only if you are signed up to a high deductible health insurance plan. You can contribute up to $4,150 if you are covered by a high-deductible health plan just for yourself, or $8,300 if you have coverage for your family. At age 55, individuals can contribute an additional $1,000.

https://www.fidelity.com/learning-center/smart-money/hsa-contribution-limits

Since contributions to this account can reduce your taxable income, if the employee in our example contributes the maximum limit for an individual i.e. $4,150 then the taxable income would reduce to $45,250 (=$60,000 – $3,600 (401k contributions) – $7,000 (Traditional IRA contributions) – $4,150 (HSA contributions)).

The good part is that, like the IRA accounts, you have until the tax filing deadline of next year to contribute to this account to get the tax savings benefit.

It is important to remember that the HSA account can be used to pay for qualified medical expenses and it is only then can you withdraw money from it tax-free. But given that health care costs will be significant by the time you retire, I am sure all this money in the account can be put to good use.

This is such an amazing account! I cannot believe there are so many tax benefits with just a single account. Moreover, you get to allot some of the savings towards health care. The first thing I will do after leaving here is open this account and start contributing to this.

Excellent! This will be a good start for you and you will thank yourself later for taking this decision. I would say that we have covered all the retirement related accounts till now that help reduce your tax bill for next year. Now, we can shift to the taxable brokerage account and talk about how the taxes can be reduced if you own this type of account.

A taxable brokerage account with any institution like Fidelity, Vanguard, Charles Schwab, Robinhood, etc. does not offer the tax advantages of the retirement accounts we discussed. However, if you have incurred some losses in the investments you made in these accounts, then you can claim deductions for these losses against any realized gains from investments and even your taxable income. This is called tax loss harvesting. Let us look at an example to understand this, say you sold a stock ‘A’ and realized gains i.e. booked a profit worth $2,000. You would have to pay capital gains tax on this profit and the tax rate will depend on how long you held the investment for. [For more details on how taxes are applied to profits from selling stocks check out this blog] Lets say, in your portfolio, you have another investment ‘B’ where the unrealized losses are $5,000. There are two things you can do to reduce your taxes:

- You can decide to sell the entire investment ‘B’ such that your realized losses are $5,000. Now, you can use $2,000 of these losses to offset the profit from selling stock ‘A’ and the rest $3,000 can be used to reduce your taxable income. Remember, $3,000 is the maximum deduction you can claim against the taxable income. The remaining losses, if at all, can be claimed in the following years.87,502/yr.

- To avoid paying taxes on the gains of $2,000, you can sell some of the investment till your realized losses are $2,000. This way your gains are offset by your losses and you do not have to pay any taxes on the gains.

I get it. This is a good way to benefit from the bad investments you made. I will try to keep an eye out for any losses in my portfolio and if I feel that I do not want to continue with those investments. Looks like we have covered both the tax-advantaged and non-tax advantaged accounts. Anything else that I need to consider for tax savings?

Yes, there are a whole bunch of things that you can look at but a lot of them are based on specific situations like how close you are to retirement, do you have dependents you need to transfer money to, etc. I will not talk in detail but will just mention a few things that we can talk about when the time comes for you. One thing that might apply to you is deductions for charitable contributions. You can claim deductions for charitable contributions. For example, you can donate your clothes or other items to goodwill and claim the fair value of the items as deductions. These will come into picture if you are itemizing your deduction and are not taking the standard deduction. This resource has a lot of good details about the limits and caveats to charitable contributions

This brings our conversation full circle to the topic of donations. I am going to read up more on that and check out how to claim value on the stuff I am donating. Thank you so much for donating your time to me! I know it will be hard to claim a deduction for that but I will be forever grateful! Have a great holiday season and I will talk to you soon!