I have a house mortgage that has about 27 years to go, which feels like a lifetime. Whenever there is some extra cash left at the end of the month I am in a fix whether I should invest that money or pay off my mortgage. The investing option sounds exciting as there is so much talk about the impact of compounding growth that can make you millions if you invest over a long period. On the other hand, paying down the mortgage seems a conservative or safe option because the upside here is not making millions but instead becoming debt free. However, after the mortgage is paid off you can invest your entire mortgage and get into the magic of compounding growth. Even though you would have more money to invest, the time over which you can invest will be less compared to if you started to invest from the beginning. Which option will give you more money over the same time period and hence is better for you is the question I want to answer. Let us listen into the conversation with Wealth Wise Owl to understand how to find an answer.

Check out these resources for more information

Should You Pay Off Your Mortgage Early or Invest? | Financial Advisor ExplainsStop Investing to Pay Off a 3% Mortgage? Here’s Why.

Should I Pay Off My Mortgage? The Math & Beyond…

Use the links below to jump to a particular section:

Details of the two options and assumptions in the analysis

Factors that decide which option is better

Scenario where paying off mortgage is better

Scenario where investing in stocks is better

Conversations with Wealth Wise Owl

Hello Wealth Wise Owl! How are you doing today on this fine morning?

Hello my friend! I am wonderful, just soaking in the sun and getting my dose of Vitamin D. It just feels so good during winter to get some natural warmth.

I am 100% with you there. I saw the sun come out and felt the urge to take a walk and soak in as much warmth as I could. This makes me feel much better than the heating inside the house. The added benefit of stepping out is that I can think better and come up with intelligent questions to ask you.

It is a win-win situation for both of us then. You get to ask interesting questions and I enjoy our conversation. What is the question you thought of on your walk today?

In recent times, I have been lucky to have some extra cash in my hand at the end of each month. I am wondering what would be the best way to use that. Should I use it to pay down my mortgage or should I invest that money?

I am glad you are in the position to have extra cash, which already means that you are making the right financial decisions. Now, on your question with what to do with extra cash, I would say that it depends on which step you are at in the order of investing.

[Check out this blog to find out the most optimal order of investing]

For example if you are at the step 3 of your order of investing, where you are have to pay down your credit card debt then the extra cash has to go towards paying down the principal of credit card debt. If you are at Step 4, then you need to put the extra cash towards building your emergency reserves and so on. I feel your question of whether to invest or pay down your mortgage would come after Step 5, where you have already saved 25% of your salary in 401k, HSA, IRA and brokerage accounts. This guarantees that your retirement is secure and then you can worry about optimizing your next dollar.

[Check out the different retirement accounts that you need for retirement]

That makes sense. I need to have my retirement secure because I cannot live off my mortgage free house. I will go back and check if I am meeting my 25% savings goal but assuming that I am, how can I decide where to put my next dollar?

If you are at the stage where you have saved 25% of your salary towards retirement, then you are in a really good spot because it gives you the freedom to optimize your wealth. We can walk through a few scenarios to understand all the factors that would affect your decision to either invest or pay off your mortgage.

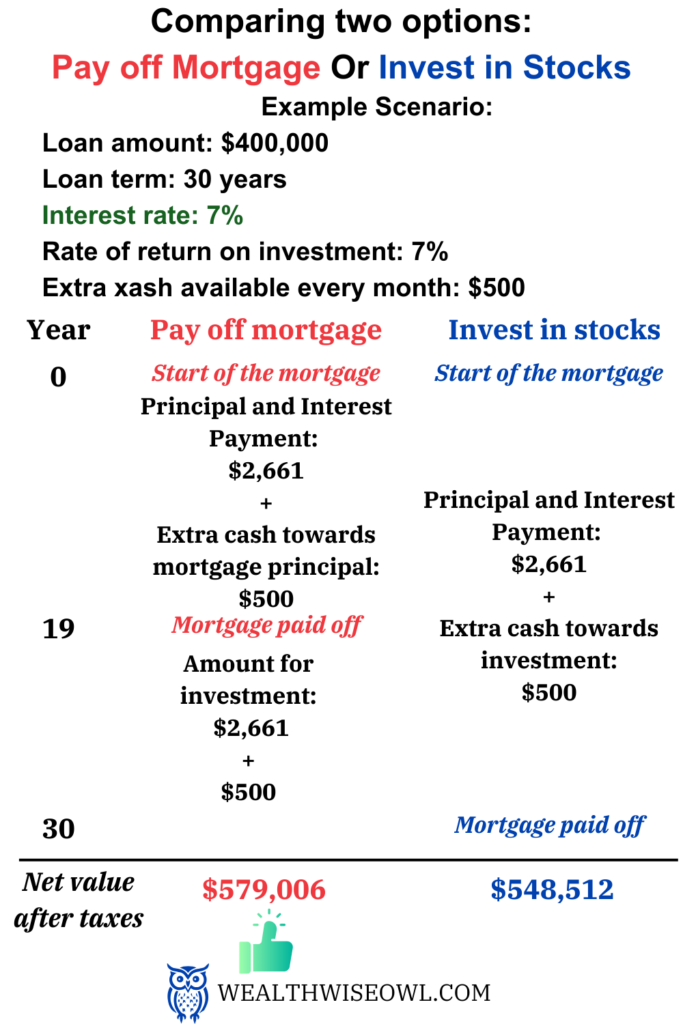

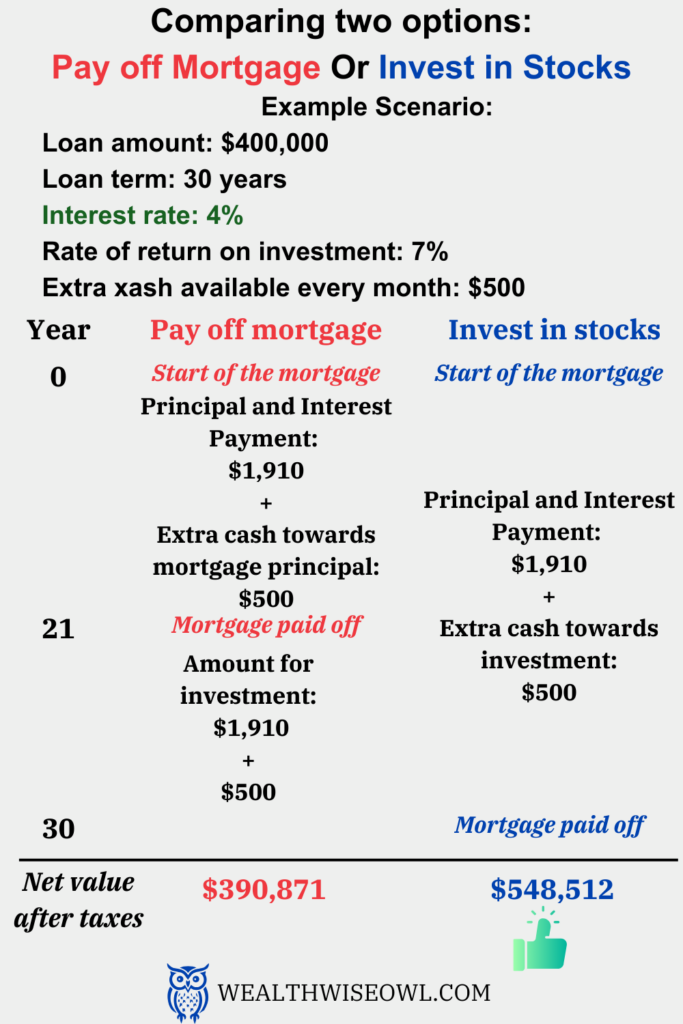

Let us first set up an example and then we can create different scenarios. If you have a mortgage of $400,000 over 30 a year loan term, we can check how different decisions affect how much money you end up with.

Below are the key factors that I feel will affect your decision:

- Interest rate on mortgage

- Rate of return on your investments

- Age and timeline for investment

That is interesting to know that there are so many factors that go into deciding which option is better. I would like to play around with these factors to see which option works better in which situations. But I will definitely focus on the situation I am in first.

Yes, once you figure out the methodology you can play with the numbers. Let us talk through the methodology to compare the two options.

Option 1 is paying the extra cash toward paying off your mortgage and once you have the mortgage paid off, you invest your entire mortgage payment plus the extra cash till your original mortgage term ends and further till retirement.

Option 2 is paying the bare minimum towards the mortgage and investing the extra cash. You would pay off your mortgage at the end of the original loan term and then you invest your mortgage payment plus the extra cash amount till retirement.

To do an apples to apples comparison of these two options we will look at the amount of money you have at the end of the original mortgage term as well as at retirement.

There are some assumptions in this analysis:

- The tax implications for the two options are the same. This would be possible if we assume we take standard deduction for taxes, so that paying mortgage interest does not give any benefits of lower taxes. Also, we will assume that the rate of return on investment is after taxes.

- We will consider investing in a taxable brokerage account, so while calculating the amount of money we end up with we will consider the long term capital gains tax on the profits made from investment.

- Throughout the loan term and up to retirement, the extra cash available does not change. The average rate of return and interest rate on loan also doesn’t change.

- To keep things simple the rest of the financial situation remains the same.

- The income limits for long term capital gains tax is assumed to increase at the rate of inflation.

Okay, I understand the two options and the fact that we will compare the net wealth after long term capital gains tax at the end of the original loan term and at the start of retirement. I am eager to get into the numbers and find out which option comes out on top.

Alright, let’s get into the numbers then. The loan amount we will consider is $400,000 and the age when you initiated this loan is 30 years.

[Check out this free excel spreadsheet to run your own numbers and compare the two options]

The principal and interest payment will depend on the interest rate of the loan and the loan term. Let’s say the interest rate for a 30 year loan term is 7% based on the current economic environment. The principal and interest payment will be $2,661.

The average rate of return from investing in a simple index fund like the S&P500 from 1928 to 2024 is about 7% after adjusting for inflation.

Let’s say at the end of every month there is $500 of extra cash available. We will consider the use of this extra cash in the two options of either paying down the mortgage or investing in a index fund like the S&P500.

In Option 1, you put the extra cash every month towards paying down the principal of the mortgage. In this case the mortgage will get paid off in 19 years, which is 11 years earlier than the 30 year loan term. In these 11 years, you get to invest the money you were paying towards the mortgage as well as the extra cash i.e. a total of $3,161.

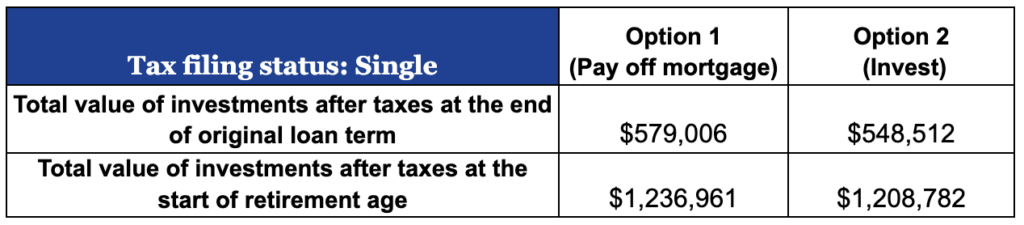

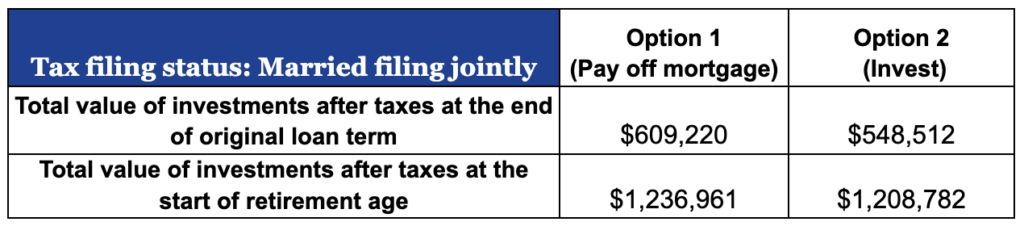

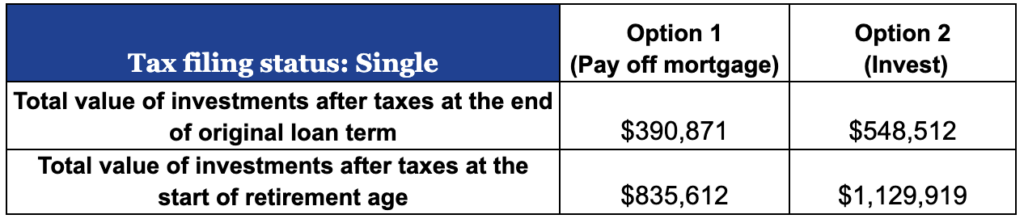

At the end of the 30 year loan term, you will have a paid off house and a total of $609,220 in investments out of which $201,424 will be profits. The long term capital gains tax will depend on the tax filing status and will be applied on the profits.

At the time of retirement, which will be at say 67 years i.e. 7 years after the original loan term. The total value of investments at the time of retirement will be $1,336,423 and the profits from investment will be $663,086.

In Option 2, the extra cash is invested in the S&P500 for the entire 30 year of the loan term while making the minimum monthly payments towards mortgage. The value of investments at the end of the original loan term will be $613,544 out of which $433,544 are profits.

After the original loan term, you can invest the mortgage payment as well as the extra cash payment till the retirement age. At the time of retirement, the value of investments will be $1,343,472 and of this amount $897,930 will be profits.

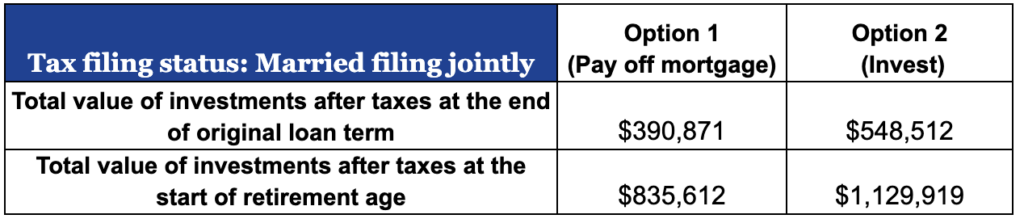

After deducting the long term capital gains tax, the total value of investments for the two popular tax filing status are

This shows that the option of paying off the mortgage is better in this scenario. There are also some intangible benefits of paying off the mortgage that cannot be put into numbers. The peace of mind from getting rid of debt is priceless. So, if you are the kind of person that values that then the advantage of paying off the mortgage first will be far greater than the $20k-$30k that you see in the numbers.

Also, we are assuming an average rate of return on investment but usually the rate of return fluctuates from year to year. So, it may happen that in a given year the investments may not grow and instead drop by 10% whereas in the next year they would grow by 20%. Therefore, it may be disconcerting to watch your investments fluctuate so much. However, with paying down the mortgage there is a guaranteed rate of return which is equal to the interest rate on the loan.

I am grateful to understand the methodology and I am sure to use the excel spreadsheet you shared for these calculations. The option to pay off the mortgage early results in $20k-$30k more than the option to invest and I can totally relate to the benefit of not having to worry about any debt. Are there any scenarios where investing would be better than paying off the mortgage?

That is an interesting question and I am sure there are plenty of scenarios where investing should be preferred over paying off the mortgage. The one scenario where I am sure investing would be better is: Rate of return on investment > Interest rate for mortgage. For example if you had purchased your house a few years back when the interest rates were low, say 4% then the comparison of the two options are below. Here, the rest of the conditions are the same as above.

Here, you can see that Option 2 to Invest is the clear winner and that too by a huge margin to tune of $200k-$300k. This means that everything being the same, a higher rate of return on investment than the interest rate on mortgage will make Option 2 more attractive than Option 1. The non tangible benefit of a higher value in investment is that it is a liquid asset that you can use for other needs or necessities. Having a paid off house will not allow you to use the equity in the house without taking on more debt or significant loss to the asset value.

Similarly, if the rate of interest on mortgage is higher than the rate of return on investment then paying off the mortgage will be a better option i.e Option 1 is more attractive than Option 2. We have already talked about the non tangible benefits of this option.

You need to remember that there are other factors too that could impact the results. These are the age at which you take the loan and the time you have till retirement. I will let you investigate the impact of these things on your own time because I know you will enjoy the aha moment when you get to the results.

I get it! A simple way to find out which option will be better is to compare the rate of return on investment against the interest rate on the loan. Whichever rate is higher, it would make sense to divert any extra cash towards that option. I am so glad we talked about this because I understood the methodology to compare the options on the same basis and understood all the factors that could influence the attractiveness of the two options.