“How much money does it take to retire?”, is a question asked frequently because let’s be honest, nobody wants to keep working forever. For the minority who want to keep working forever, they will be happy to know when they can just work for fun and not worry about supporting their livelihood i.e. become financially independent. The answer to this question is frustratingly simple and vague – “It depends on you!”. This is also the reason why retirement is part of “personal” finance because it is very specific to your personal situation and choices. The traditional definition of retirement is to work till your retirement age but the popular F.I.R.E movement changes that. F.I.R.E stands for “Financial Independence, Retire Early”, which is a movement towards aggressive savings to become financially independent and have the option to retire early. Even though the traditional retirement and F.I.R.E movement are two contrasting thoughts about retirement, the common need they have is knowing if you have enough to retire or at least become financially independent.

I talked to the Wealth Wise Owl about how to arrive at this magic number and really hope that I am not too far from it. So, regardless of whether you want to work till your retirement age or are avid followers of the F.I.R.E movement, this conversation will be of interest to you. Even though I use the word “retirement” in my conversation, it is equivalent to being financially independent because I do not see any point in retiring if I am not financially independent.

Use this FREE Excel sheet to calculate your magic retirement number

See all the infographics at a glance HERE

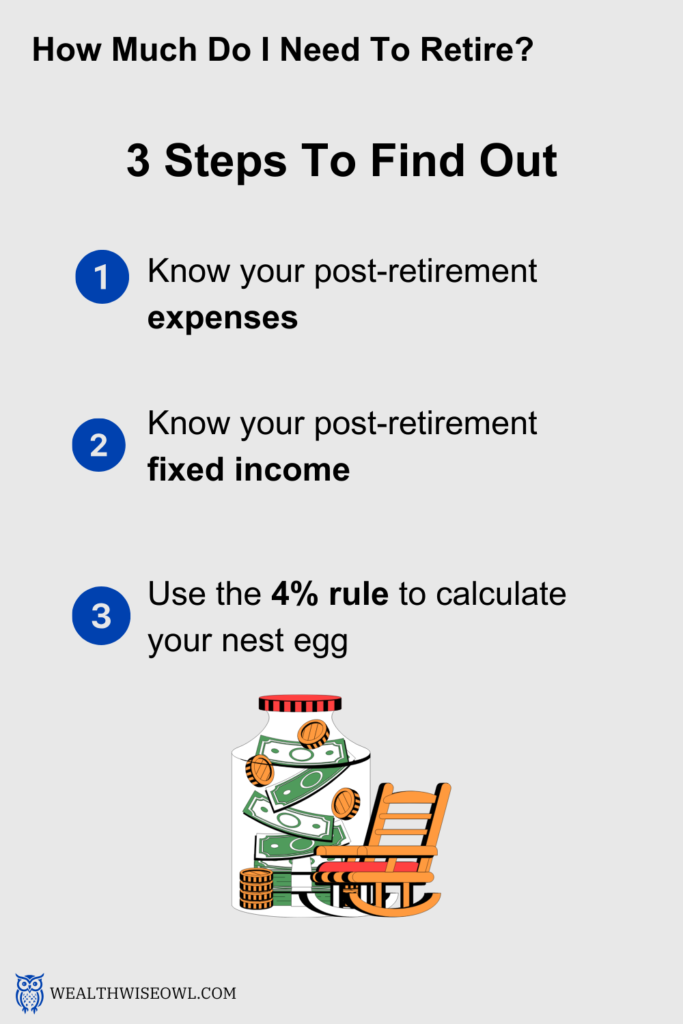

There are three key steps to get to the magic number and if you would like to jump to specific topics in the conversation, use the links below –

- Know your expenses during retirement

- Know your fixed income during retirement

- Calculate if you can meet the deficit between expenses and fixed income

Conversations with the Wealth Wise Owl

Hi WWO, good to see you relaxing on this nice day! If I didn’t know better, I would have assumed that you recently retired from your job!

Hellooooo, yes, I am aware of the effect retirement has on humans and not at all jealous of how long it takes to get to that stage. But I can sense that you have retirement on your mind today, so what are you thinking about?

You are indeed Wise my friend, because I have been thinking about how do I know I am ready to retire or when can I NOT worry about actively working to meet my living expenses?

This is a really good question to think about because the answer to this will ensure peace of mind and reduce the worry of not having enough in retirement. I think it will also give you a specific goal to keep working towards, which you can enter as a destination in the GPS of your financial journey and then decide the best route to get there.

I really like the analogy of having a GPS for my financial journey and can’t wait to find out what destination I need to enter. Where do I even begin?

Actually, it is a simple three step process. The first step is to arrive at the number of how much your expenses will be during retirement. This is the same as coming up with a budget but for your future self.

Well, it is hard enough to keep a track of my current expenses and now I have to predict what they will be for me in the future! I hope they sell a crystal ball on Amazon because there is no way I can tell what I will be spending 20-30 years from now.

I agree that this is not an easy task and it will be easier to calculate this number closer to your retirement. But fear not, I will tell you some ways to estimate your expenses during retirement. They may not be exact but at least you do not have to go chasing after a crystal ball that does not exist yet!

Okay, Phew…I am down for getting a ballpark number for now. How do I estimate it?

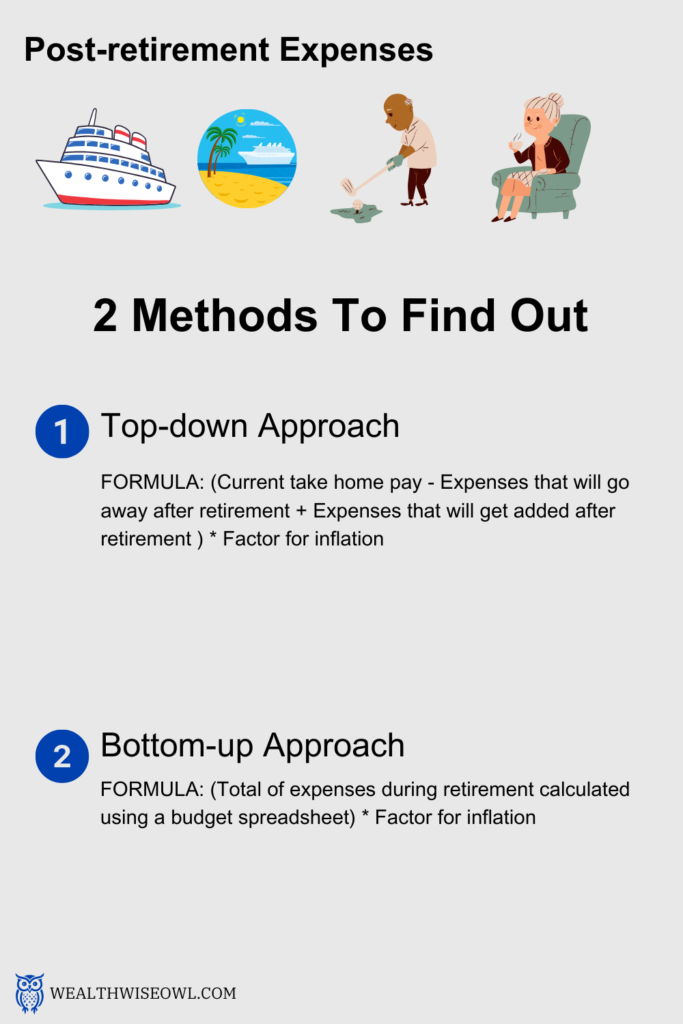

There are two main approaches to calculate your expenses [Use this link to download a free excel file to calculate your nest egg]

- Top-down approach

This is a little less work but will also be less accurate.

- You need to start with your current take home pay, which is easy to check based on what is deposited in your bank account. The take home pay usually covers your current living expenses as well as any savings you might be doing.

- Next, you subtract any expenses that you will not have during retirement. For example, you might not need to pay the principal and interest part of your mortgage, so that can be subtracted. Also, you might be saving some money for your retirement, so that can also be subtracted since you are in retirement now.

- Then you add any additional expenses you think you might have during retirement. For example, you might want to travel more or buy a car that you always wanted to have. You should use the current prices of these expenses.

- Now the number you end up after the above steps will need to be adjusted for inflation since you have been dealing with the current prices in your calculations and these wont remember the same when you retire.

To put simply,

Top-down approach future expenses = ( Current take home pay – Expenses that will go away after retirement + Expenses that will get added after retirement ) * Factor for inflation

2. Bottom-up approach

This is a lot more work and you will have to spend time with a spreadsheet or notepad in this approach. Basically, you will have to write down different categories of expenses and then put a number next to it. Again, since you do not know what the price of those items will be during retirement, just use the current prices and then later adjust for inflation. There are a lot of helpful spreadsheets available online to list down your expenses for budget planning, which will make this task easier.

Bottom-up approach = (Total of expenses during retirement calculated using a budget spreadsheet) * Factor for inflation

[A couple of YouTube videos that I would recommend to watch on these two approaches. They also have links to spreadsheets for calculating your monthly budget :

How Much Do You Need to Retire in 2023?

How Much You Should Save For Retirement]

I am tempted to use both the approaches and see how different the results are. But I feel since I am still a long way from retirement, I will use the top-down approach because predicting my detailed expenses will be equally inaccurate at this point. Now that I have this number, what is the next step?

The next step is to know what is your fixed source of income or in other words, the income you will not need to generate from your savings like retirement accounts, brokerage accounts, etc. This fixed income includes your social security benefits, income from any rental properties you may own, etc. You qualify for social security if you have at least 10 years of taxable income where you pay FICA taxes. How much social security you will get is a more complex topic so let’s talk about that later. Meanwhile, you can check out your benefits at ssa.gov

[Use this link to download a free excel file to calculate your nest egg]

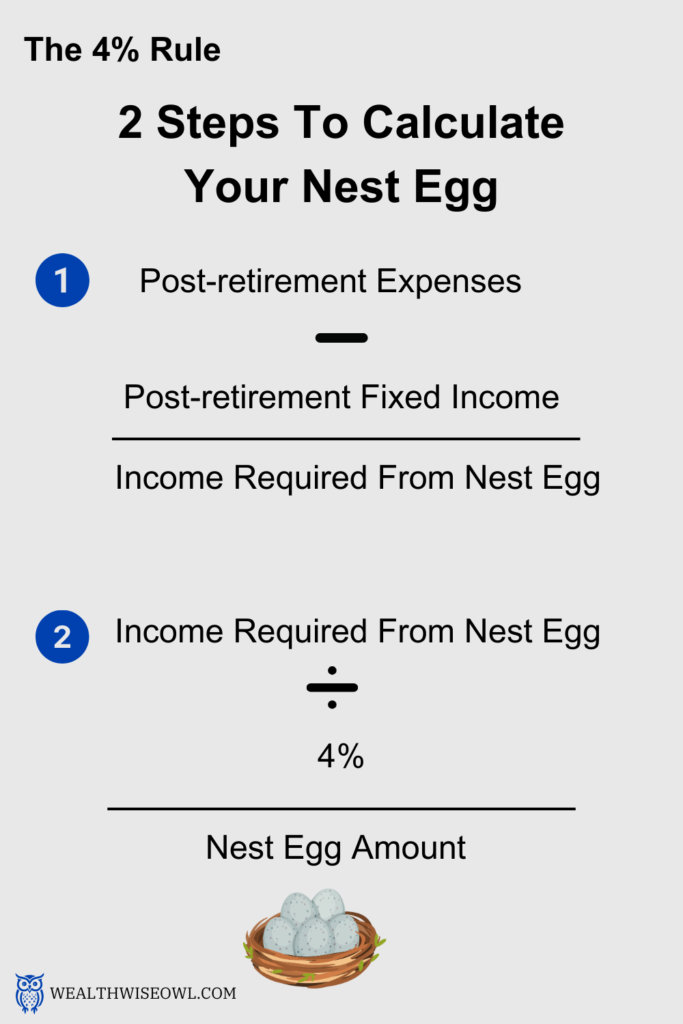

This income, after adjusting for inflation, can be subtracted from the expenses you calculated from the first step and you will end up with a number you need to earn from your savings. If you want to be really conservative, assume that you will need to meet all your retirement needs from your savings. This will be an aggressive goal for the amount you need to save for retirement but it will be a guaranteed peace of mind.

Interesting point about social security benefits, I will come back to learn more later. The aggressive savings goal seems like a steep challenge but I would rather aim high when it comes to retirement. I do not want to work a day more than I need to and if having high goals is the way to go, so be it. We are at the last step now, this is the big reveal of the magic number, right?

Yes, this is the last step of the process and will give your final destination number to plug into your Savings GPS. The first two steps helped you get to the number you will be withdrawing from your accumulated savings. Another way to arrive at this number is to use the Fidelity’s income replacement rate guidance, which says that you will only need a certain percentage of your pre-retirement income during retirement. This percentage depends on what age you decide to retire and is again a very rough gauge on how much your retirement needs will be. [Please check out this YouTube video for more information on Fidelity’s income replacement guidance – Fidelity’s Rule of 45% | How Much Do I Need To Have Saved Up To Retire?]

Once you have the income you need from your retirement savings, you can calculate how big your retirement nest egg should be. [Use this link to download a free excel file to calculate your nest egg] Keep in mind that your retirement savings can be in multiple accounts like 401k, IRA, taxable brokerage, etc. [Check out The Ultimate 401(k) Guide For Beginners] Now, your nest egg has to be big enough such that you can keep withdrawing for your expenses without ever running out of money. This rate at which you withdraw is called the safe withdrawal rate and is popularly referred to as the 4% rule.

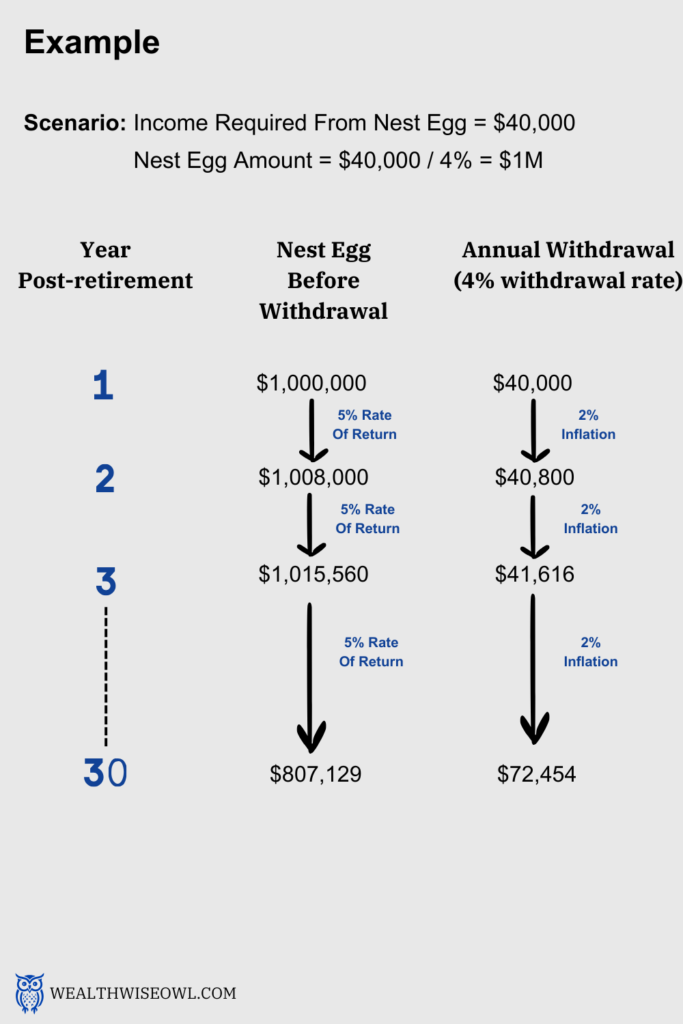

A study conducted by CFP Bill Bengen in 1994, estimated the safe withdrawal rate to be 4%, adjusted for inflation, over a period of 30 years at least. This means that if you have a 1 million dollar nest egg then you can safely withdraw $40,000 in the first year, $40,800 in second year (= $40,000 *1.02, for 2% rate of inflation) and so on. Based on this strategy you will not run out of money for at least 30 years. The important caveat here is that your savings need to be invested in a portfolio that has a higher rate of return than your rate of withdrawal and inflation rate combined. Based on the study that was conducted, a 50% portfolio in US large cap stocks and the rest in US Intermediate term Treasuries, had a non zero account balance over any 30 year period in our history, which includes all the booms and busts we have had so far. So, your investment portfolio is very important to decide on a safe withdrawal rate. Also, this does not take into account any taxes or fees that you would have to pay on your withdrawal and assumes that it will be paid from the 4% withdrawal amount. Another assumption in this study is that you will withdraw a fixed amount every year adjusted for inflation but that is not always the case since your needs might change from year to year. There are a lot of such gaps in the 4% rule and it is supposed to be considered a guideline rather than a rule. Remind me to talk about just this 4% rule someday, especially on how it was arrived at and some of the assumptions in this study.

It was important for me to give you a flavor of the 4% rule so that you understand it is just for an estimate and not a perfect number to live by. With that being said, you can calculate your nest egg by simply dividing the number you got after the first two steps by 4%. So, if you find out that you need to generate $50,000/yr from your savings then you need to have a nest egg worth $50,000/0.04 = $1.25 Million. Now, this looks like a huge number but remember I showed you how saving a small percentage of your salary in your 401k account every year can make you a millionaire [See the The Ultimate 401(k) Guide For Beginners]

[Please check out a few YouTube videos that I liked about the 4% rule

How Much $ Do You Need to Retire? The 4% Rule for 2023

Is It Time to Update the 4% Rule?

Can YOU Afford Retirement? | 4% Rule Explained | Safe Withdrawal Rate]

I am glad that you showed me how to get to these massive numbers in my 401k accounts, because I do not feel intimidated by these 7 figure numbers. Guess what, I am off to find my coordinates to my retirement destination and come back to get your wisdom on ways to get there.

[…] Read the detailed post here […]