Have you heard the phrase “It is too good to be true”, well it definitely applies to the Health Savings Account aka the HSA. In my quest to maximize tax savings and savings for retirement, this account stood out. Besides this it also helped save for the most important thing in anyone’s life, which is health. With this much build up you would be curious to know what exactly is a HSA and what this hype is all about. I am sure as you read on you will reach the same conclusion as me that this is the best account ever. Let us hear into the conversation with the Wealth Wise Owl.

Here are some resources that I used to learn more:

What Is An HSA And How Does It Work? | Money Unscripted | Fidelity Investments

The Hidden Truth About an HSA (Health Savings Account)

Why Should I Use a Health Savings Account (HSA)?

https://www.investopedia.com/articles/personal-finance/120715/why-hsas-appeal-more-highincome-earners.asp

Use these quick links to jump to a section of your interest

- How and where to open a HSA account

- Eligibility for a HSA account

- Contribution limits in a HSA

- Three tax advantages with a HSA

- How to invest your money in a HSA

Conversations with Wealth Wise Owl

Hellooo my friend! Top of the morning to you!

Hi there, you seem to have a cold because I can clearly hear it in your voice. How are you feeling?

You got that spot on! I have a runny nose and sneeze far too frequently for my liking. I think it was the change of weather that caused this to me, despite all the layers I wore to protect from cold. Now I am off to the pharmacy to get some cold medicine.

Oh my..it is never fun to be sick, especially at the start of the year when you are rearing to go on to new things. It is at times like these that the words “Health is Wealth” ring so true because you cannot enjoy anything without good health. On the note of wealth, I hope you have a Health Savings Account to pay for medical expenses.

I know we have talked about Checking account and Savings account but that is the first time I have heard of a Health Savings Account. I am curious to know what it is and why you recommend me to have one?

I am glad you asked this because I am sure you would fall in love with this account. As the name suggests a Health Savings Account is mainly used to store money that you can only use for qualified medical expenses but after age 65 it can be used as a Traditional 401k or Traditional IRA account. [Check out this blog to learn more about retirement accounts]

You can contribute to this account only if you have a High Deductible Health Plan (HDHP), which are health insurance plans that have relatively lower premiums but higher deductibles than the Low Deductible Health Plan (LDHP). Whether or not you should go for a HDHP or LDHP depends on your health situation and anticipated medical expenses. But if you go with a HDHP then you definitely need to have a Health Savings Account.

Wow, an account that is dedicated to saving for your health, I like the sound of this. I think I have a High Deductible Health Plan, so will definitely look into opening this account. How and where can I open this account?

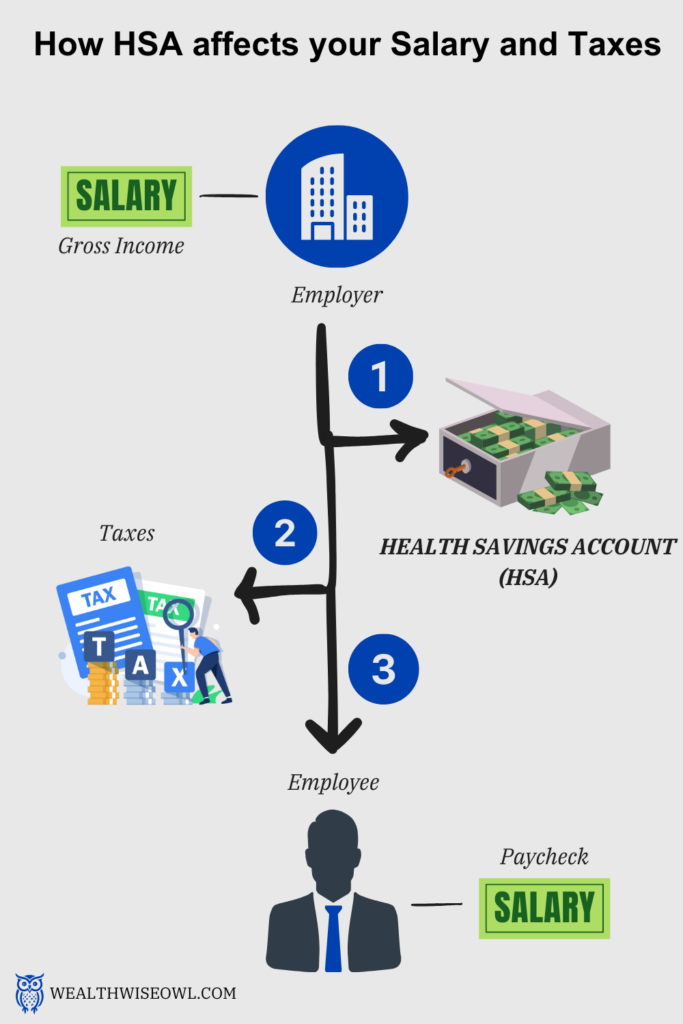

These accounts just like the 401k accounts can be provided by your employer but you can also open them yourself. You can talk to your HR department to check if your employer has partnered with any institution for the HSA because that is where they can make contributions from your paycheck directly to this account. However, if your employer has not partnered with an institution or you want to open another HSA, you can choose an institution of your liking to open this account. https://www.bankrate.com/banking/savings/best-health-savings-accounts/

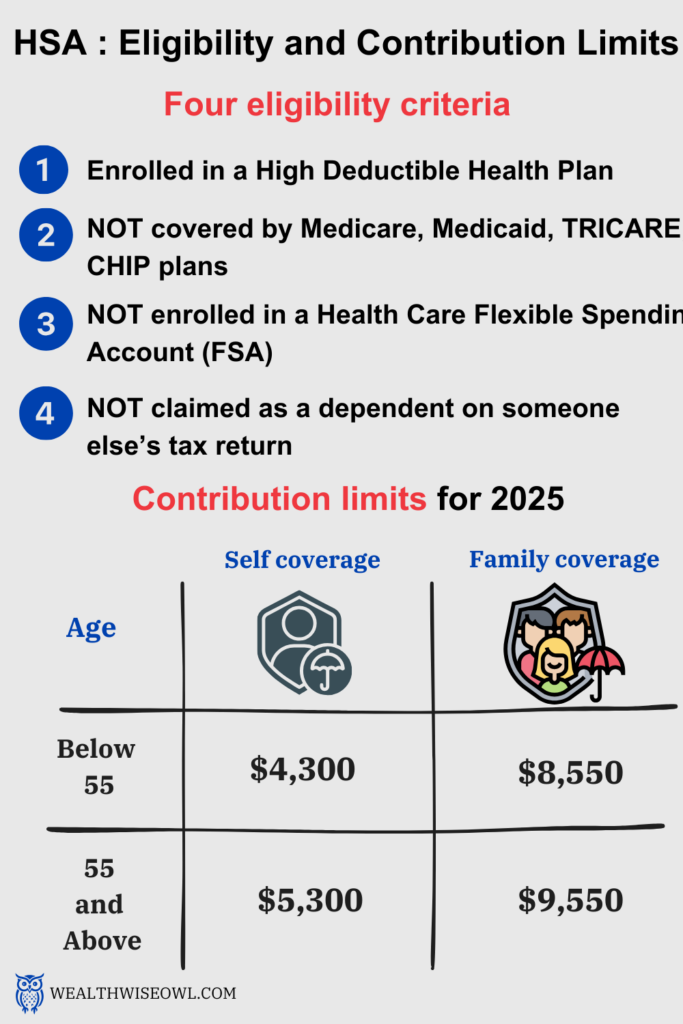

Remember there are certain eligibility criteria you need to meet to open this account (https://digital.fidelity.com/prgw/digital/hsaeligible):

- You cannot be claimed as a dependent on someone else’s tax return

- Enrolled in a High Deductible Health Plan

- Not covered by any of these plans – Medicare, Medicaid, Children’s Health Insurance Plan, TRICARE

- You or your spouse are not enrolled in a Health Care Flexible Spending account (FSA)

It is so cool that you can open a HSA online easily once you know you are eligible to enroll in one. I know I am going to open one as soon as I get home. Can you contribute as much as you want in this account?

Unfortunately, there are annual contribution limits to this account but the good thing is that there are no income limits on who can contribute. For the year 2025, contribution limit is $4,300 for self-only coverage and $8,550 for family coverage. People 55 and older can contribute an extra $1,000 as a catch up contribution. These limits change every year just like they do for the other retirement accounts.

HSA is better than a Flexible Savings Account (FSA) because you can carryover all the money that you do not spend unlike a FSA where you have to spend all the money or you will lose it.

You can decide the when and how much you should contribute by considering the order of investing that we talked about. This will help you decide where to prioritize contributing your money.

That’s good to know and something I will keep in mind. You said that I will fall in love with this account, are we getting to the part where you tell me why?

I was keeping that as a suspense but seeing you eager to know, I cannot wait any longer. The reason you will love this account as would anyone else is because it is a triple tax advantaged account i.e. it helps save on taxes in three different ways and everybody loves to save on taxes.

- The amount you contribute is deducted from your taxable income, so you contribute your pre-tax dollars and save on taxes. This tax savings part is just like the one you have in a Traditional 401k or Traditional IRA account. [Check out this blog to learn about the tax savings in 401k and IRA accounts]

- The contributions you make to the HSA grow tax-free. You may wonder how the growth part happens and that is where HSAs are amazing. You can invest the contributions you make to a HSA in stocks, bonds, ETFs, etc.

- Finally, you can withdraw money from this account tax-free if you use that money for things that are not qualified medical expenses. Do remember that if you use the money for non qualified medical expenses then you would have to pay a 20% penalty as well as pay taxes on that money since it would add to your taxable income. After the age of 65, the penalty goes away but you still need to pay the taxes on withdrawals for things that are not qualified medical expenses.

If you remember our conversations about the 401k and IRA accounts, you can see that HSA combines the good aspects of both Traditional and Roth accounts in terms of tax savings. Isn’t that amazing?

It is truly amazing! I can see why you were so confident that I would love this account. I did not know you can invest the money you contribute to a HSA. This would mean that you can grow your money as you would in a brokerage account. How great is that! How do you recommend investing the money in this account?

That is a great question and the answer is the same for any investment account – it depends on your risk appetite.

Option 1: One option that I recommend is to keep some amount in your HSA uninvested which you can use for emergency health expenses. This uninvested cash can be equal to your highest deductible amount in the insurance plan because that is the maximum you will need to pay for your emergency expenses. The rest you can invest in ETFs that track certain indexes like S&P500 so that you do not take huge risks but can still make average market returns.

Option 2: The other option is to invest all the money in your HSA so that you have more money growing tax-free. You can pay your medical expenses from your checking or savings accounts. Remember to save the receipts of your expenses so that when you withdraw the amount of money later, it can be tax-free.

Let us do a thought experiment on the potential growth in a HSA. In the best case scenario, you would invest all your contributions and let’s assume you aim for the average market returns. Let’s say you maximize your contributions in the year 2025 for family coverage i.e. $8,550 annually or 712.5 every month and you maintain this for the next 30 years. You would end up contributing $256,500 over 30 years and if we assume average annual market returns of 7%, this money would grow to $807,073. This is roughly growth of 3 times the investment you made, which is huge!

https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

The average amount of money an individual can expect to pay for medical expenses is $165,000 and $330,000 for a couple.

So, you can see that you would actually need to save a lot of money for your medical expenses and HSA is the best way to save for this.

I am amazed at the amount you can have in your HSA account if you just contribute up to the annual limits consistently every year. I really like your first option of maintaining a certain amount of uninvested cash, equal to the highest deductible, for medical emergencies and then investing the rest in some index fund ETFs. This way I hope to save enough for my medical expenses.

Thank you so much for sharing this! I am already feeling better and might not even need the medicine now! Hopefully I am in perfect health when I see you the next time.