The IRS has started to accept income tax returns and I am sure you must be getting bombarded with ads from tax filing softwares to start filing your returns. I know this is not as exciting as a spring sale announcement or a car sales event but something we need to do regardless. Taxes are the least favorite topic that anyone wants to talk about let alone begin the process of paying them. One of the main reasons I believe is how complicated the tax system is and not just in the US but in many parts of the world. I personally dread the idea of filing taxes because of the numerous documents it involves and all with weird numbers as their names, which makes it even more dreadful. It was only recently that I was curious to know what tax bracket I fall in and wanted to find this out on my own instead of using the tax softwares. It was one of those things which I dove into without thinking twice and probably that’s why I went ahead with it. At the end of it, I can say I am more comfortable with taxes because I have a basic understanding of how taxes are calculated. I am no way close to spitting out Tax forms names off the top of my head or giving tax advice but enough to estimate taxes for simple situations. I would like to share what I learnt and if your tax situation is simple enough you can at least get a ball park on how much taxes you owe. This in no way replaces the accurate tax calculation that is either your CPA, tax professionals or tax filing softwares so please consult them when you actually file your taxes. But if you are a curious person like me and want to uncover the mystery behind taxes, listen to the conversation with the Wealth Wise Owl.

Conversations with Wealth Wise Owl

Hello my friend! How are things looking from up there? Are you seeing a lot of happy faces in the new year?

Hello! Well, it is hard to see faces because everything is wrapped up in mufflers and caps but I can definitely feel the hustle bustle of people starting the year with a lot of energy.

That is good to know. There is a fresh new list of things to do and I think this is the peak of everybody’s energy after a good break. I am also optimistic on making good progress on my to do list and the one I am most fearful of is filing taxes. For me taxes mean a ton of paperwork and reading terms that are confusing to say the least. Can you please help me with that?

I think that is one fear everyone has and something they would want to avoid if they could. But it is equally important to go through the process because that is how public amenities get maintained and there is good infrastructure for everyone’s benefit. I agree that things can be made more simple and I can tell you a bit on how taxes are calculated in very simple terms. We usually fear the things we do not understand, so hopefully our conversation will alleviate some of your fears.

I would really appreciate that! I think if you can go over how taxes are calculated then in the process I will be able to get a sense of what different things mean in the tax forms. I do not want to be a tax expert but some basic knowledge will go a long way in helping me.

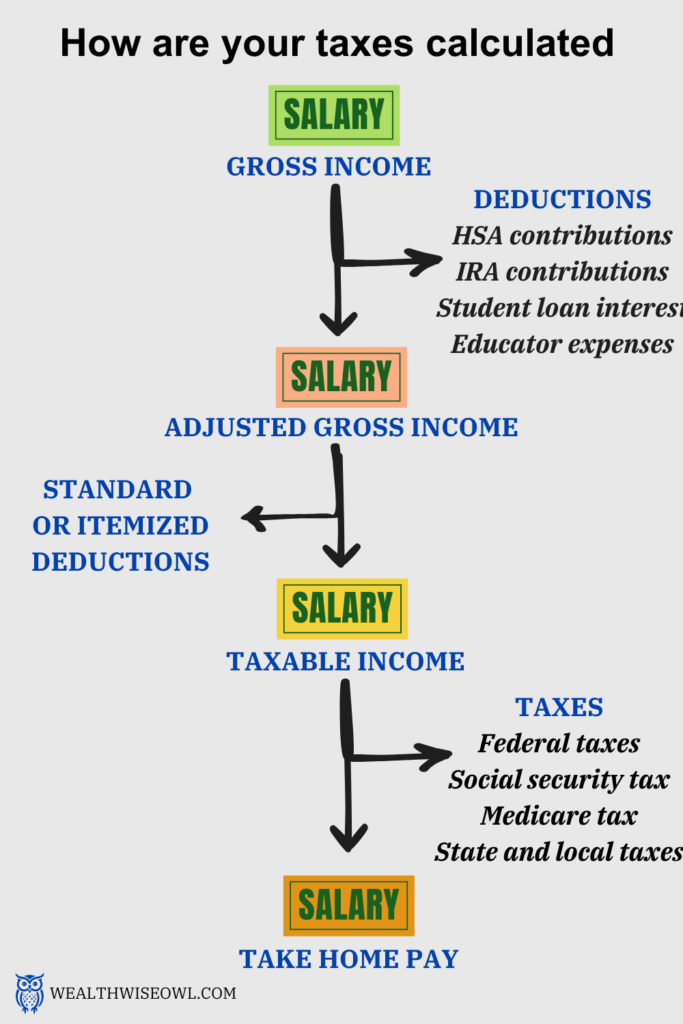

Yes, I am sure you will come out better than before after this. First, you need to understand that filing tax returns simply means letting the IRS know how you earned, what your expenses were and if you qualify for any tax deductions and/or tax credits. Based on the types of your income, you will have to use different forms to communicate the same type of information. All this information is then taken into account to calculate what your taxable income is and then determine how much taxes you owe. If the taxes you owe are less than the taxes that are collected automatically from your paycheck, then you will get a refund but if you have not paid enough then you would be asked to pay the remaining amount. Another thing that you would keep seeing throughout the tax filing process is your tax filing status. This depends on your personal situation and based on that you get different deductions, so this is the first thing that you need to determine in the tax filing process but it is probably the easiest thing to do.

Reporting income is a key part of filing taxes. This income can be from various sources based on your situation. Some of the common sources are wages from the employer, tips, income from side jobs, capital gains from selling investments, etc. All this income would add up to your Gross income.

https://www.nerdwallet.com/article/taxes/federal-income-tax-return

Now, there are some deductions that you can reduce from the Gross income. These deductions are good because it will help reduce the amount of taxes you need to pay.

These deductions are different from the Standard deductions or Itemized deductions that you would have heard often. Some of the common deductions are:

- Contributions to a Health Savings account [Check out this blog to learn more about Health Savings Account]

- Contribution to a Traditional IRA account [Check out this blog to learn more about IRAs and other retirement accounts]

- Student loan interest deduction i.e. you can subtract the interest paid on your student loan up to a certain amount if your income meets the specific criteria

- Educator expenses i.e. money spent out-of-pocket by teachers on class or classroom costs. Again there are limits on how much you can claim in deductions.

All of these deductions are subtracted from the Gross income and calculated the Adjusted Gross Income (AGI). AGI is important because it is used to determine if you qualify for any additional deductions, tax credits and even some states use this to calculate your state taxes.

Adjusted Gross Income = Gross income – Deductions

From this Adjusted Gross Income, you can either subtract the standard deduction or itemized deduction, depending on whichever is greater, to calculate your taxable income. A standard deduction is a flat reduction based on your filing status whereas an itemized deduction is taking deductions for individual items, which are all added up.

Taxable income = Adjusted Gross income – Standard/Itemized deductions

https://www.investopedia.com/terms/t/taxableincome.asp

Standard deduction: Usually if people do not have a lot of itemized deductions or if they want to keep things simple, they choose standard deductions. For 2024, individual tax filers can claim a $14,600 standard deduction (up to $15,000 for 2025) or $21,900 (up to $22,500 for 2025) if they are heads of households. For married couples filing jointly, the standard deduction is $29,200 (up to $30,000 for 2025). So if you are filing under “Single” status in the year 2024 and your AGI is $50,000, then your taxable income will be $35,400 (=$50,000 – $14,600) with standard deduction.

Itemized deductions: If you have paid for certain things during the year then you can claim deductions for those and it may be higher than the standard deduction. Some popular things that qualify for itemized deductions are:

- Property taxes and mortgage interest

- State and local taxes paid

- Charitable donations (limited to a percentage of AGI)

- Educational expenses paid for qualified higher-education expenses

- Unreimbursed medical bills that exceed 7.5% of your AGI

This taxable income is used to determine where you fall in the federal tax brackets and hence you can calculate how much federal taxes you owe but more on that later.

Wow! I did not know there are so many versions of an income on a tax form. But now I understand how they are calculated and that each of them is used for a different purpose. I think once the taxable income is calculated we get to the actual tax calculation part, correct?

Yes, we will talk about the tax calculation part now. In the US, there is a progressive tax system for federal taxes where your tax rate increases as your taxable income rises. This type of tax system puts less tax burden on those who earn relatively less so that they have more to spend on essential goods and services.https://www.investopedia.com/terms/p/progressivetax.asp

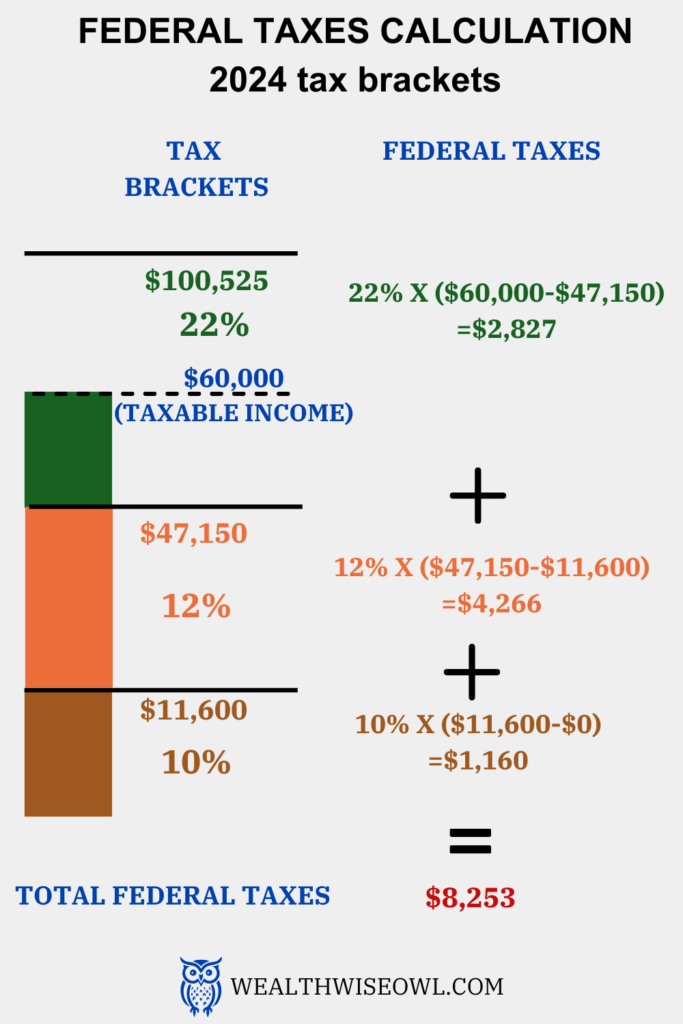

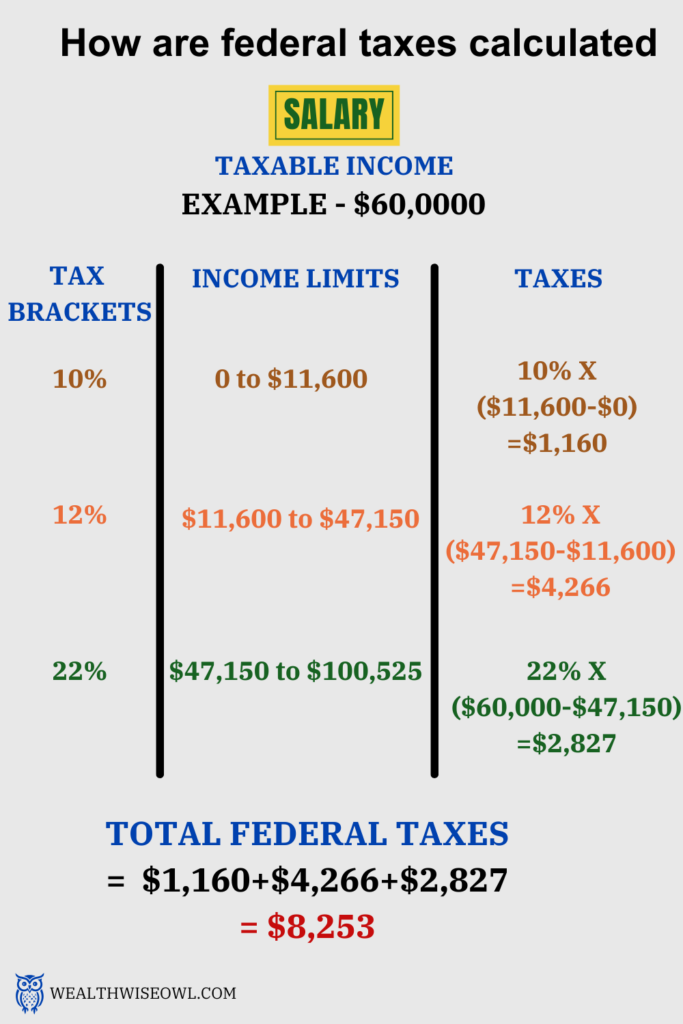

Based on your taxable income, in 2024 you can end up in one of the seven tax brackets with rates of 10%, 12%, 22%, 24%, 32%, 35% and 37%. The table below shows the tax brackets and the range of income for each tax bracket. It is easier to understand how the federal taxes are calculated using an example. https://taxfoundation.org/data/all/federal/2024-tax-brackets/

If in 2024, you had a taxable income of $60,000 and “Single” filing status, then you would fall into the 22% tax bracket. This DOES NOT mean that you would have to pay 22% taxes on all your income. You just have to pay the tax rate on the income that exceeds the minimum threshold for that particular tax bracket.

In this example, since $60,000 is higher than the income range for the 10% tax bracket, you pay 10% taxes on $11,600 of your taxable income, which amounts to $1,160.

Similarly, $60,000 exceeds the 12% tax bracket, so you pay 12% taxes on the entire income range in this bracket i.e. 12% of $35,550 (=$47,150 – $11, 600) which is $4,266.

Now, $60,000 does not exceed the income range for the 22% tax bracket, so you only pay taxes on the amount that exceeds the minimum threshold for this tax bracket i.e. $47,150. So, the income on which taxes need to be paid at 22% rate is $12,850 (= $60,000 – $47,150), which is $2,827.

So, the total federal taxes to be paid are calculated by adding up the taxes to be paid in the different tax brackets i.e. $1,160 + $4,266 + $2,827 = $8,253.

This shows you that as you earn more income you fall into higher tax brackets but that does not mean that your entire income is taxed at that higher tax rate, it simply means that the next dollar you earn will be taxed at that rate. the number of tax brackets, tax rates and income range for tax brackets are set every year by the IRS.

This is quite an exercise to look at the tax bracket table and figure out which bracket you fall into. I am relieved to know that it is not the entire taxable income that is taxed at a single rate. But these are just the federal taxes, right? There are other taxes too that I see in the tax form.

You are right! You also need to pay the Social Security taxes and Medicare taxes but these are directly withheld from your paycheck. https://smartasset.com/taxes/all-about-the-fica-tax

Social security tax rate is 6.2% and it is paid on your gross income not the taxable income. There is an income limit for this tax, it is $168,600 for 2024 and $176,100 for 2025. So you do not need to pay the Social Security Tax on income above $168,600 in 2024.

Medicare tax is also a flat tax rate of 1.45% on the gross income. However if you earn more than $200,000, then there is an additional 0.9% on the amount that exceeds $200,000, so a total of 2.35% on the amount that exceeds $200,000.

Let us consider an example to calculate these taxes. Let us say your gross income is $80,000.

Social security tax that will be withheld from your paycheck during the entire year will be 6.2% of $80,000 i.e $4,960

Medicare tax withheld over the entire year will be 1.45% of $80,000 i.e.

$1,160.

State and local taxes on individual income also need to be paid but this depends on the state you belong to. Also, each state decides on what they consider as the taxable income, whether to use a progressive tax rate or flat tax rate, etc. These things are so specific to the state that you would be better off to read more on this separately.

I like how easy it is to calculate the FICA taxes where you do not have to look at a table or anything. I believe these are the taxes that will help us later during our retirement. I also appreciate you explaining all the terms and nuances of how the taxes are calculated. I will feel more comfortable now going into the tax season and filing my taxes for sure.