If you are someone who thinks about maximizing their retirement savings and which accounts to invest in the you are not alone. I have been thinking about this for a while and want to make sure that the decisions I am making today about my retirement savings will give me the maximum rewards in the future. This way my retired version can give a good pat on the back to my today’s version while putting his feet up on a nice cruise. I used this as the motivation to investigate more into the topic of maximizing my retirement savings and the first question that I decided to answer was – which one is better: Traditional 401k or Roth 401k? Since the time I have had my 401k account, the question of whether the Traditional is better or Roth has bugged me. If you also have the same question then read on about the conversation with Wealth Wise Owl for some useful information.

Here are some resources that I used to learn more:

401k or Roth 401k? Which is Better?

Roth vs. Traditional: What Is Best For YOU?

Please use the links below to jump to a particular section

Simple thumb rule to decide between Traditional 401k Vs Roth 401k

Example with calculations to decide between Traditional 401k vs Roth 401k

Conversations with Wealth Wise Owl

Good morning my friend! It is a chilly morning today, hope you are keeping warm there.

Helloo! Nice to see you. It is indeed very cold today and my feathers are just enough to keep me warm. Any colder than this and I would have to put on layers like you.

You are so lucky! I had to spend a good 15 minutes to layer up and will have to take it down when I go back home. The good thing about cold is that hot coffee tastes even better! I plan to get some and work on selecting my retirement savings options.

Wow that is some important stuff you are planning to do, glad you have some good coffee to keep you company. Do you know what choices you will make on your retirement plan?

Not really and that is why I am grateful that I ran into you. I would really like to know your thoughts on how to approach this selection. The thing I need to make a selection on is my employer’s 401k plan, where I have to decide on what percentage of my salary I would like to contribute and whether that contribution should go to a Traditional (pre-tax) account or a Roth (After-tax) account.

I can definitely share my thoughts on this and hopefully it will help with your selections. First just a refresher on what the Traditional and Roth 401k accounts are would be good.

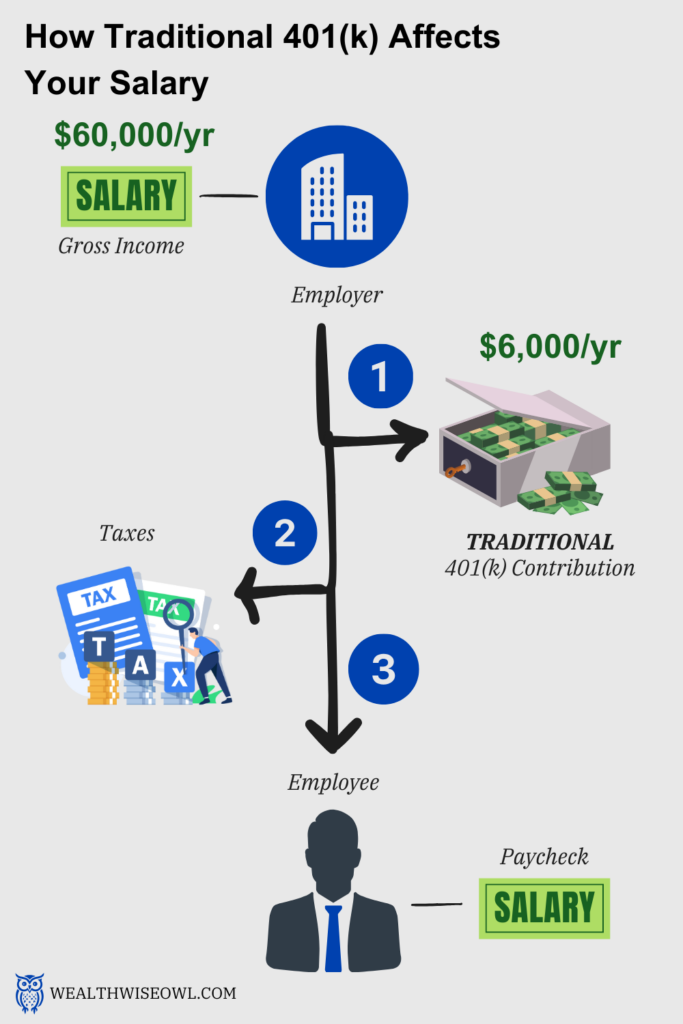

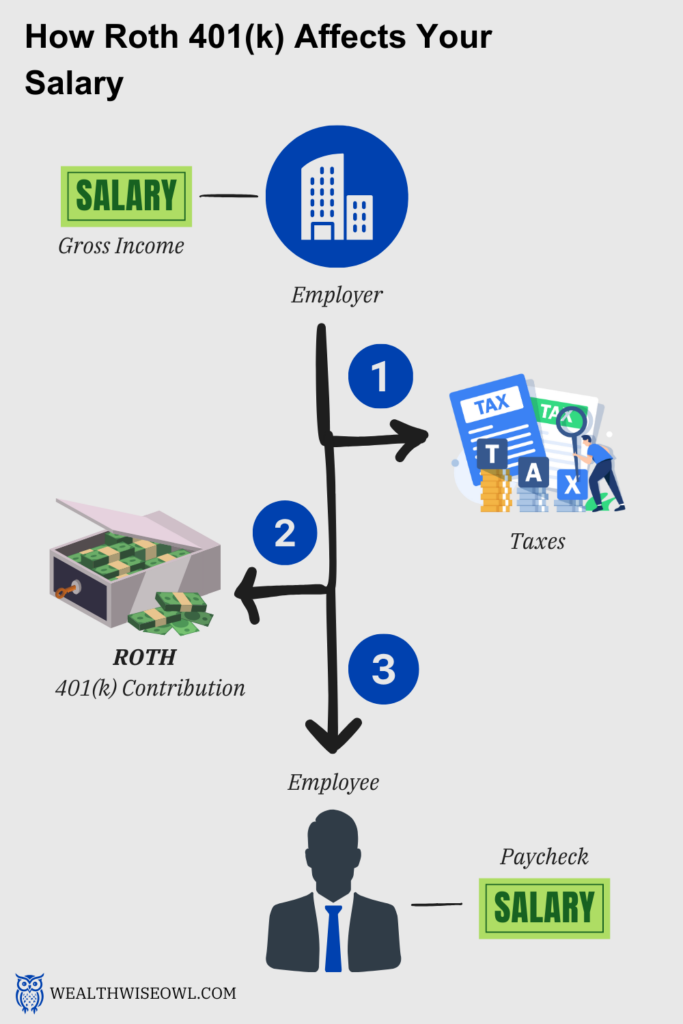

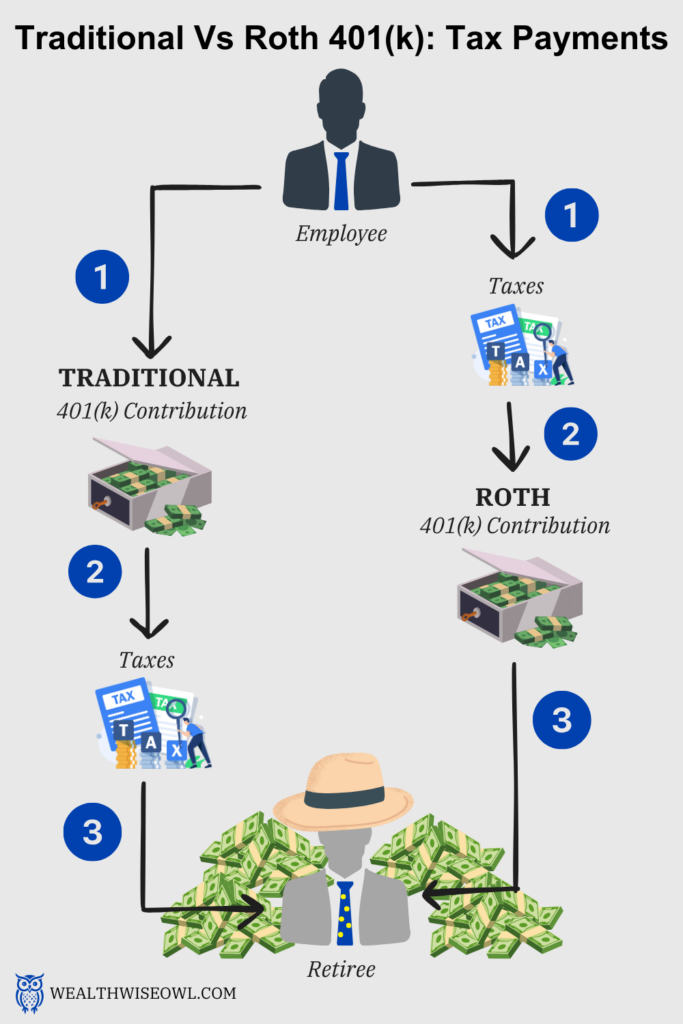

Traditional 401k account: This account is funded by your pre-tax dollars, which means that the amount you contribute to this account reduces your taxable income. This means that you can get tax savings and the higher your marginal tax bracket is, higher that savings amount would be. All the money you put in this account can be investmented into equities/stocks that are part of your 401k plan. These investments grow tax-free. When you retire and take the money out from this account, you need to pay taxes based on the amount you withdraw and the tax rate at that time.

Roth 401k account: In this account, the amount you put in comes after paying taxes, so this does not give you any tax savings today. However, when you withdraw the money from this account after your retirement, you do not pay any taxes then. Just like in the Traditional account, you have equities/stocks to choose for investments, which grow tax-free.

[Check out this blog to get more details on the different types of retirement accounts]

Thanks for the refresher! I know we had talked about these accounts before but there are so many details that I tend to forget. The easy way for me to remember is that the tax treatment is the main difference between the two accounts. A Traditional account is about saving taxes now and paying later whereas a Roth account is about paying taxes now and savings taxes later. How is that for a strategy?

That’s excellent! This is a neat way to remember the main difference between the accounts. One more thing that is related to 401k plan is the employer match, which may or may not be offered by your employer. If it is, then it is a great way to get some free money. Basically, your employer matches your contributions to the 401k account up to a certain percentage and at a certain rate. For example, your employer match could be a 50% match up to 3% of your salary. This means for every dollar you contribute to the 401k account, up to 3% of your salary, your employer will contribute 50 cents. For example if your salary is $60,000/yr and say you contribute 3% of your salary, which is $1,800, then your employer will contribute $900 (50% of $1,800) to your 401k account. Remember that the employer match always goes to the Traditional 401k account even if you make all your contributions to the Roth 401k account.

Awesome, I will keep a look out for the employer match because this sounds like a sweet deal to get some extra money in my retirement accounts. I am sure to atleast contribute enough to get the employer match and anything more than that will depend on my budget.

That is a great strategy to plan your investing. You should definitely aim to get the employer match. I think the next big decision would be on whether you should make your contribution to the Traditional account or the Roth account?

[Check out this blog for an optimal order of investing]

In simple terms, it makes sense to invest in Roth 401k if you expect to be in a higher tax bracket during your retirement than your current one. This means that you pay lower taxes now and save paying higher taxes during retirement.

You should contribute to Traditional 401k if your current tax bracket is high and at retirement you expect to be in a lower tax bracket. This will help you save on taxes now and pay less taxes during your retirement.

That is an easy way to remember where to contribute. The main objective is to pay less taxes so that you have more money to spend on yourself. Can we go through a case study to understand which is a better option? I think numbers will help drive the point home.

Yes, let us take an example to talk through how you can think about comparing the two options. The example is very simplistic and may not directly apply to you but it will guide you to analyze the options on your own later.

[Download this free excel spreadsheet to look at the calculations and play with it yourself]

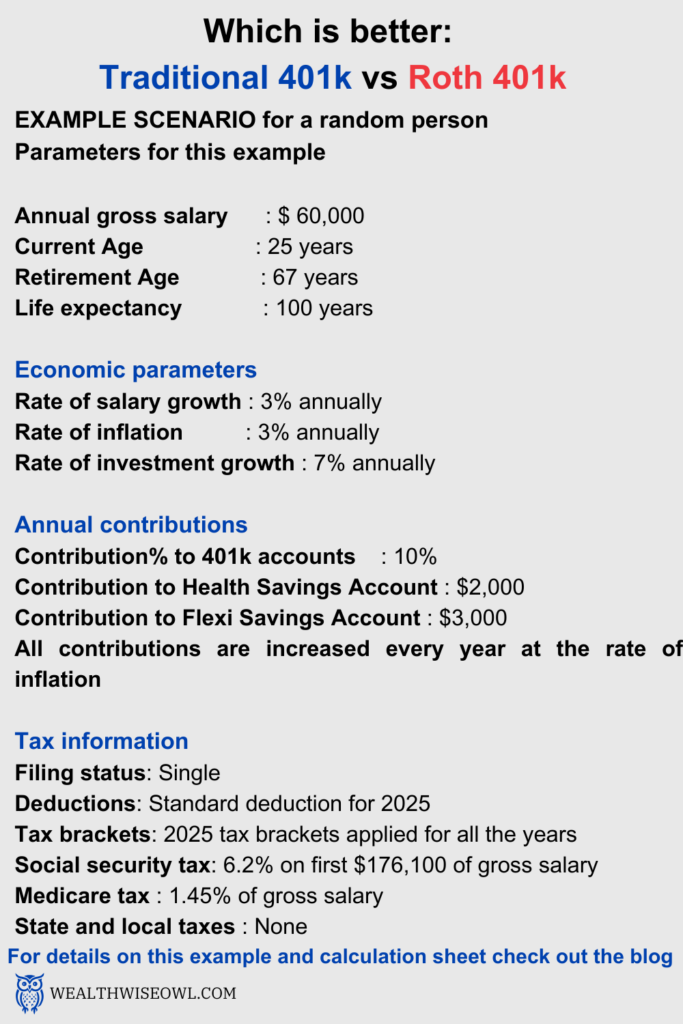

In this example let us assume we have a person who is 25 years old and has a gross salary of $60,000/year. This person aims to retire at the age of 67 and has a life expectancy of 100 years. Let us set up this example by listing all the parameters we will use and you can change these based on your own analysis.

Economic parameters

Rate of salary growth : 3% annually

Rate of inflation : 3% annually

Rate of growth of investments in 401k accounts : 7% annually

Annual Contributions

Contribution% to 401k accounts : 10% of gross salary

Contribution to health saving account : $2,000

Contribution to Flex spending accounts : $3,000

All the contributions are increased every year by the rate of inflation and we assume that they will not exceed the contribution limits for that year.

Tax Information

Filing status: Single

Deductions : Standard deduction, which is increased every year at the rate of inflation

Tax Brackets : 2025 Tax brackets and they are assumed to be the same over the years, which is highly unlikely but it is impossible to predict what they will be in the future

Social security tax: 6.2% on first $176,100 of gross salary

Medicare tax: 1.45% of gross salary

State and local taxes : None

Other Assumptions

- Living expenses : Assuming that 401k is the only saving and rest of the salary after paying taxes i.e. take home pay, is used for living expenses

- The living expenses after retirement is equal to the take home pay just before retirement plus the amount paid to the health related accounts. These expenses grow at the rate of inflation every year.

- The amount withdrawn from the Traditoinal 401k account after retirement is always above the required minimum distribution (RMD)

- We assume all the living expenses will be funded from the 401k accounts and not HSAs, Borkerage accounts, etc.

Below are some important steps to compare if contribution to a Traditional 401k or Roth 401k would be better in the above example:

Step 1: To do an apples to apples comparison for these two scenarios, we need to make sure that the amount of money left after contributing to the 401k accounts is the same in both scenarios. This would mean that the amounts contributed to the 401k account will be different in the two scenarios since one is before taxes and the other is after taxes. You can take a look at the excel spreadsheet to see how different they are over the years. For the first year, the amount contributed to the Traditional account is $6,000 but that contributed to Roth account is $5,280, which is less than the Traditional account because the contribution is made after paying taxes.

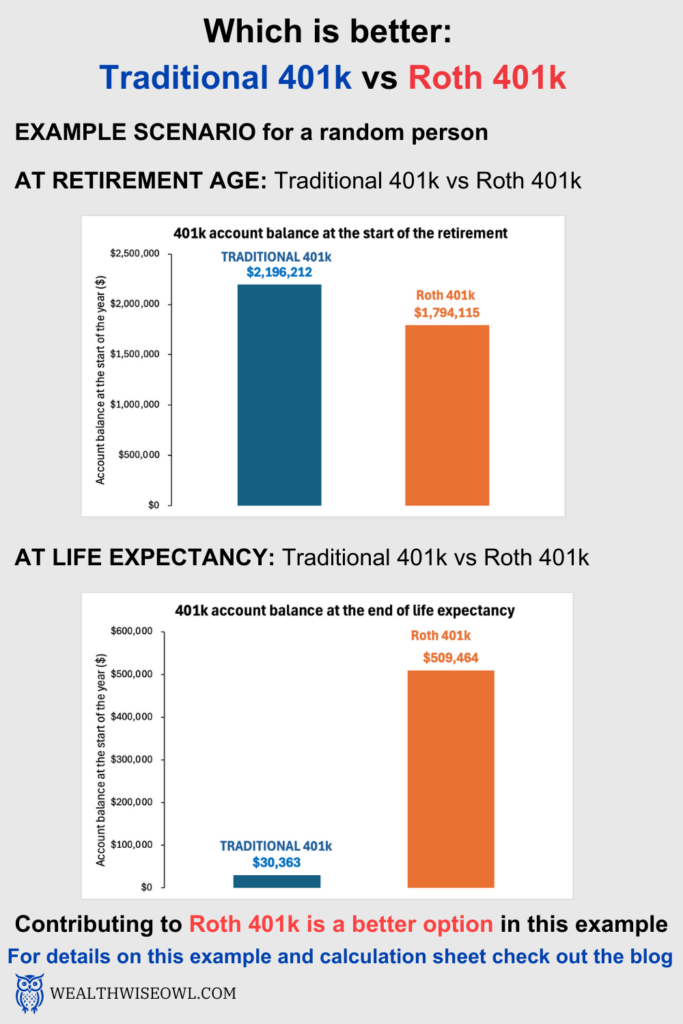

Step 2: Calculate the amount of money in the 401k account at the retirement age by assuming that the investments in the account grow at a fixed rate every year. This way you will end up with a final account balance in both Traditional and Roth 401k accounts at retirement. In this example, the amount in Traditional account is $2,196,212 and Roth account is $1,794,115. Even though the Traditional account has a higher amount, we need to remember that taxes need to be paid on any withdrawals from this account so the effective balance will be lower.

Step 3: We need to calculate how long the money in the 401k accounts will last after retirement. The account in which money lasts longer will be the better account. After retirement, we do not have any salary and no social security/medicare taxes. The withdrawal from the 401k accounts is the only source of income and it needs to match our living expenses. We assume that the living expenses will be equal to our take home pay just before retirement along with money paid to the health related accounts. For the Traditional 401k account, we need to withdraw more than what we need since we also need to pay taxes but for Roth 401k account we withdraw the exact amount that we need. In our example, the balance in the Roth account at the age of 100 years is $509,464, whereas, the Traditional account balance is only $30,363.

This suggests that contributing to the Roth account is better than Traditional for the person in this example. Another important lesson here is that this person should have contributed more than 10% to 401k accounts or have other forms of savings to be able to withdraw more than required for basic living expenses.

There are two major caveats to this result:

- Here, we assumed that we will always withdraw above the required minimum distribution. However, if that is not the case then we will have to withdraw more than what we have assumed and pay higher taxes. This might reduce the balance in the Traditional account faster.

- Another big caveat here is that the tax brackets throughout are the same as the year 2025 but that is highly unlikely. If the tax brackets get adjusted such that this person has to pay more taxes after retirement for the same amount of taxable income then the Traditional account may deplete faster. On the other hand, if the person had other forms of savings like a brokerage account, then withdrawals could be strategized to reduce the amount of taxes and the Traditional account would have depleted slower.

Thank you for going over this example. I have understood that there are several dimensions to this analysis and it is not a simple answer that will apply to all the situations. I will run the numbers for myself and try to figure out if one option is better than the other. I am also tempted to try contributing equally to both. This way I am not putting all my eggs in one basket and can benefit from both.

That could be a good strategy too and you can also run numbers if a 50-50 contribution to both the accounts will result in a higher account balance at the end.

Overall, I think this is a very simple example and has several assumptions involved which can change based on a number of factors which we cannot predict. Hence, if you are serious about getting a definitive answer it is recommended to talk to a financial advisor or professional who has advanced softwares that can run several scenarios with different parameters/assumptions and tell you which strategy would be better across the majority of those scenarios.

I will definitely consider reaching out to an expert and going over my situation. At least I am knowledgeable enough to ask the right questions and hopefully understand their reasoning for choosing one option over the other. As always I have enjoyed our conversation today and look forward to the next one!