I bought my house in December 2022 and my interest rate was 6.625% on a 30 year mortgage. I have friends who bought their house in 2020-2021 and had interest rates on their mortgage as low as 3%. The main thing that changed between 2021 and 2022 is the decision of the Federal Reserve Bank to increase the Federal Funds Rate. The Federal Reserve Bank wanted to lower the rate of inflation by increasing the rate and the hope was that they will start cutting the rate once inflation is below 2% or the unemployment numbers start to increase, whichever comes first. With that in mind, I knew that sometime in the future, I will be able to refinance my mortgage to a lower interest rate. I followed the news related to Federal Funds Rate very closely and kept a track of the 30 year mortgage rates. It was the most recent rate cut in December 2024 that I thought I would be able to get a great deal on the 30 year mortgage rates since the Federal Funds rate was in the 4.25-4.5% range, much lower than my mortgage rate. To my great disappointment the mortgage rate actually jumped up and that is when I realized that I did not have a good handle on what was going on. I decided to read more into it and understand what actually governs the 30 year mortgage rate. I definitely know much more than when I started and would like to share what I learnt. Let us talk to the Wealth Wise Owl to learn more.

Below are some resources that I looked at to gather information:

https://www.fanniemae.com/research-and-insights/publications/housing-insights/rate-30-year-mortgage

https://www.investopedia.com/ask/answers/033115/what-are-differences-between-treasury-bond-and-treasury-note-and-treasury-bill-tbill.asp

https://www.bankrate.com/mortgages/how-interest-rates-are-set/#how-rates-are-determined

Use the links below to jump to specific sections

- Mortgage Backed Securities (MBS)

- 30-year mortgage rate calculation

- 10-year Treasury notes

- Primary-Secondary mortgage spread

- Secondary mortgage spread

Conversations with Wealth Wise Owl

Hello my friend! Nice Santa hat you have on there. Merry Christmas!

Merry Christmas my friend! I am enjoying the festivities this holiday season and the hat also helps me keep warm.

Excellent choice! I love this time of the year and enjoy all the food there is to eat with family and friends. Not to mention decorating the Christmas tree with presents for everyone. The gift I need this Christmas is a low 30 year mortgage rate!

I keep watching the news but have no clue on how and when the mortgage rate will go lower. Could you please help me understand that?

Yes, of course! It is an important subject and is not talked a lot about because it looks complicated and frankly is not an exciting subject. But for someone who is looking to buy a house or even refinance their existing mortgage, this could be the most interesting topic!

You are so correct! I feel people are more excited to talk about the stock market, the next Apple or Microsoft but anything that relates to mortgage rates is pushed to the background. I am guilty of doing this at a number of occasions but since I am going to be affected by it in the near future, I really want to understand mortgage rates better.

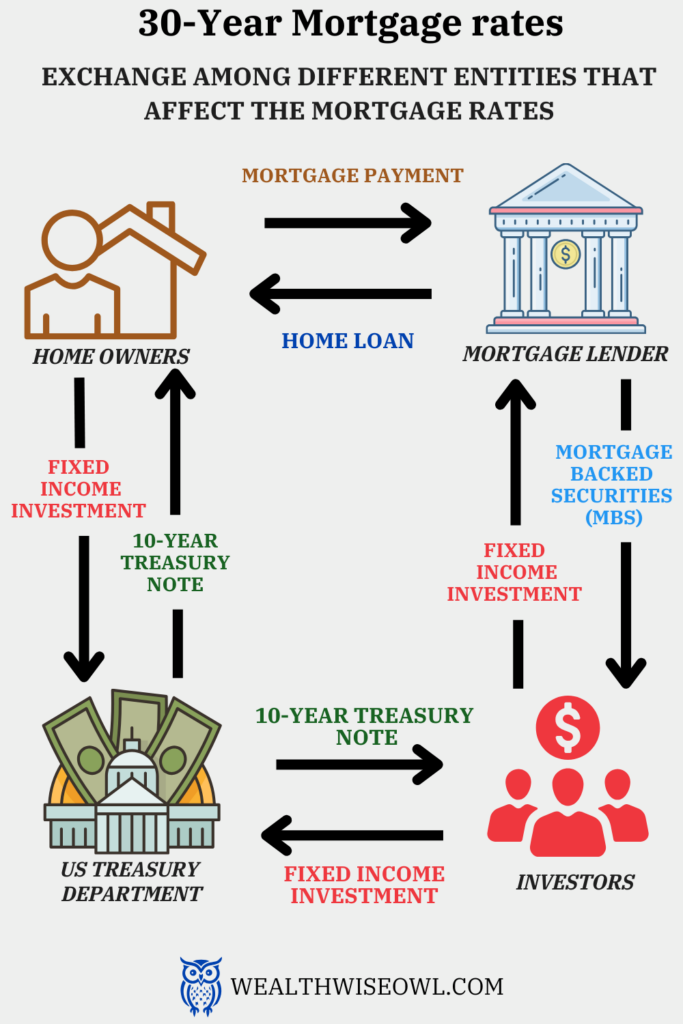

Okay, let us then begin talking about this. To understand how mortgage rates are determined it is important to know what goes on behind the scenes and what all parties are involved. When you apply for a mortgage at your local bank or with a mortgage lender, the bank offers you a 30 year mortgage based on what they do behind the scenes. Your mortgage is clubbed with other mortgages that have similar characteristics like the amount of loan, credit scores, term of loan, interest rate, etc. Then these groups of mortgages are converted into securities, which is similar to a stock or bond, that is available for investors to buy. These securities are fixed income investments that offer periodic income over a certain number of years. The income that they provide comes from the mortgage payments for the group of mortgages. Since these securities are based on the mortgages, they are called Mortgage Backed Securities (MBS).

Let us take an example to understand this better. Let us say that you are granted a $4,00,000 loan at 7% interest rate for 30 years. Your lender has all the details about your income, debt, credit score, type of house, etc. The lender also has granted similar house loans to a number of other people and some of them have very similar details like yours in terms of income, debt, credit score, etc. For simplicity, let us assume there are 99 more house loans that are similar to yours. All these loans are clubbed together to make a total of 100 loans that are alike in nature. There will be monthly mortgage payments for all these loans, which can be thought of as recurring income for the lender. The lender would consider this an asset, like a business, since it is generating an income. As we know a lot of businesses offer a chance for investors to get a share of their income by offering corporate bonds that have a %yield and/or shares that have dividends also expressed as %yield. Similarly, the lenders offer investors a share of the income from mortgage payments by offering mortgage backed securities that have a %yield associated with them. Or another way to look at it is that they are raising money from the investors to give out mortgage loans and then giving periodic payment to investors as a return on their investment based on the %yield. It is this %yield on the MBS that is one of the factors that determines the interest rate that the lender would offer on the mortgage. For example a 5% yield on a mortgage backed security would mean if someone buys $1000 worth of MBS, then they would get $50 (=5% of $1000) every year.

To offer a 5% yield on the MBS, the lender would have to charge at least 5% interest rate on the mortgage to be able to generate the required amount of income from the loans. The lender adds some more points to the 5% to account for the processing fees of the loan, which includes the profit they want to make, to determine the final mortgage rate they can offer. This is why you get different mortgage interest rates from different lenders because the processing fees they charge are different.

Just like there are different types of stocks and bonds that have ratings based on their quality, MBS are also classified based on their quality and have different ratings.

I have never looked at the house mortgage process as a business. But now I get the picture when I know who all is involved in the process. Basically, the lenders serve as the middle man between the home buyer who needs a loan and an investor who is looking for a fixed income investment. The lenders promise a %yield to the investors if they buy the MBS, which are like stocks/bonds, and then add some processing fees percentage points on top of that to come up with a mortgage rate. Hope I understood this correctly.

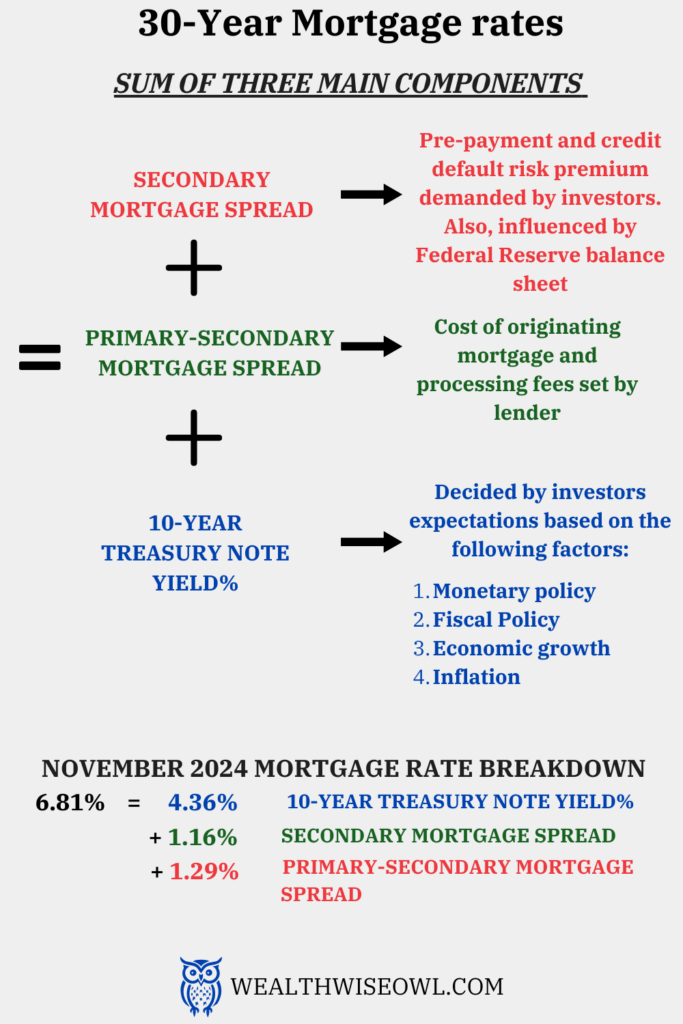

I could not have summarized that better. You hit the nail on the head in identifying the lender as being the facilitator for the deal between the homeowner and the investors. In technical terms the difference between the MBS yield and mortgage rate is called the primary-secondary mortgage spread. Between 1995 to 2005, this spread has been 0.5% on an average. After the housing market related Financial Crisis in 2008, this spread has increased to 1.01% on an average due to increase in the processing costs of the loan caused most likely by stringent requirements in approving loans to avoid another crisis.

That is totally understandable! I would rather have a slightly higher processing cost than another of those housing market fiascos that we had in 2008. I get that the mortgage rate is 0.5-1% higher than the MBS %yield but what determines the MBS % yield?

Great follow up question! The short answer to that is the 10-year Treasury note. Here is the long answer. Since MBS is an investment opportunity for fixed income, it competes with other fixed income investments like bonds. Therefore, it has to provide competitive yields compared to other bonds available to be attractive for the investors. You have to understand that it is in the interest of the lender to make the MBS yields attractive because selling MBS to investors is how they make money. Therefore, to be competitive, they benchmark the MBS yields against the most reliable bonds available in the market i.e Treasury Bonds. Specifically, the 10-year Treasury note (more specifically a blend of 5, 7 and 10-year Treasury notes are evaluated) is used to benchmark since an average mortgage term is about 10 years. The US Treasury securities – bills, notes, bonds – are considered to be the most safe and reliable option for fixed income investment because it is guaranteed by the US government and it has been more than a century since the US government has defaulted on its debt. However, the mortgage lenders are not as reliable since they have defaulted before (read the 2008 Financial Crisis). Hence, investors demand a bit more incentive in terms of higher yields to make up for the higher risk in buying MBS from the lenders. The technical term for this extra incentive over the 10-year Treasury note yield% is called Secondary mortgage spread. There are two types of risks that the lenders have to consider while offering the MBS yield% –

- Credit risk – As we discussed before, there is a risk that the home owner defaults on their mortgage due to unforeseen circumstances like economic downturn, personal emergencies, etc. This could create a default risk for the MBS if enough home owners default on their loans.

- Prepayment risk – Even though the mortgage rate term for a 30 year mortgage is 30 years, there is a chance that this mortgage can be paid off early either due to refinancing, moving to a new house, paying off the mortgage early, etc. This poses a risk to the MBS since they are based on the income from mortgages lasting 30 years.

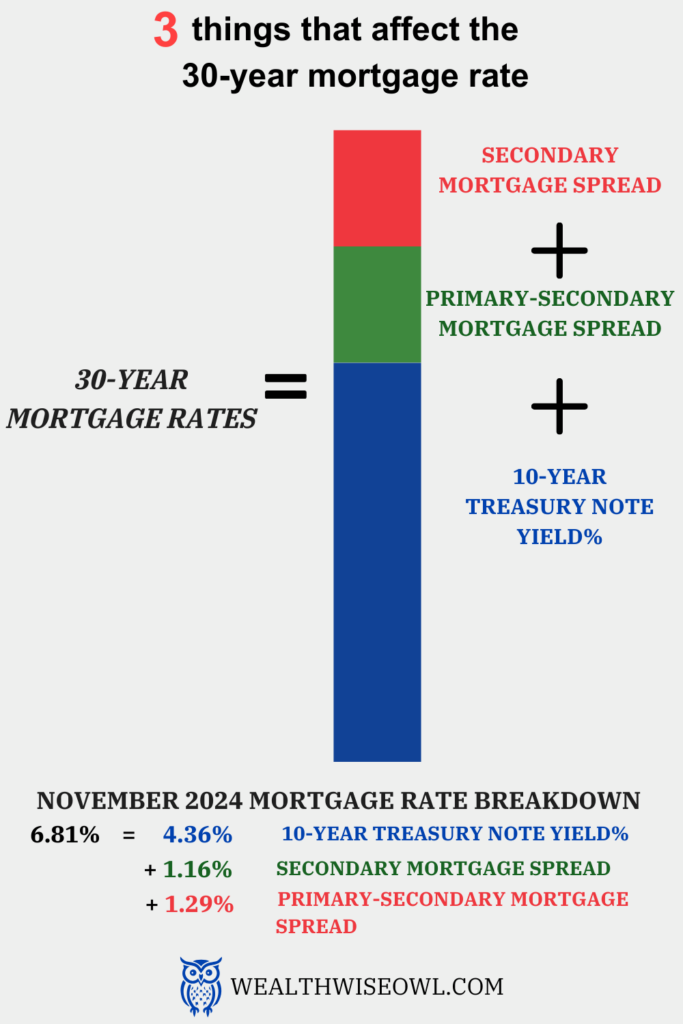

Okay, that’s some great information. From what I understood, the MBS yield% is some additional percentage points added to the 10-year Treasury note since they are a more riskier fixed income investment. Overall, what I can say is that the mortgage rate is the yield on 10-year Treasury note added with the primary-secondary and secondary mortgage spreads.

Mortgage rate% = Yield% on 10-year Treasury note + Primary-Secondary mortgage spread + Secondary mortgage spread

Amazing! I like how you created an equation out of all the things we just talked about. It is easier to understand this mathematically. Just like we talked about some numbers about how high the primary-secondary mortgage spreads, the secondary mortgage spreads were on average 1.4% from 2022-2024, 0.71% between 2012-2019 and 1.17% between 1995 to 2005.

One thing that influences this number is also influenced by how much MBS the US Federal government has on their balance sheet. During the financial crisis, the Federal Reserve had to buy a majority of the MBS as part of “quantitative easing” to stabilize the mortgage interest rates and the financial markets. Since they were buying out of necessity and not like a typical investor looking for profit, they did not demand a high premium over the 10-year Treasury note. Therefore, the secondary spread stayed low. However, more recently the Federal Reserve has stopped buying the MBS as part of “quantitative tightening”. As a result of this private investors are deciding the secondary mortgage spread. The way mortgage interest rates are going up even though the Federal Funds rate is getting cut, suggests that the private investors are demanding a higher risk premium over the 10-year Treasury note. The data says that the way the US Federal Government manages the MBS on their balance sheet has a major effect on the secondary mortgage spread and hence the mortgage rates.

I see, so it seems like the mortgage rates are about 1-3% higher than the yield offered by the 10-year treasury note. Now, I think the last piece of puzzle is what decides the yield on the 10-year Treasury note?

You are absolutely right, the yield% on the 10-year Treasury note is the last piece of the equation. This number is based on an online auction that is held every month on the US Treasury Department website. There is competitive bidding on the price and the yield% of the Treasury notes and bonds. So, you could say that it is the investors that determine the yield% of the US Treasury notes. Below are some factors that investors look at and its impact on their expectations:

- Inflation: Inflation eats away the buying power of money and to preserve the buying power, investors look for investments that have returns higher than at least the inflation. This expectation of higher returns in a high inflation environment also applies to the bonds, like the 10-year Treasury notes. Hence, the yield% from the 10-year Treasury note increases in a high inflation environment.

- Monetary policy: This includes the Federal Funds Rate set by the Federal Reserve Bank and their policy for future rates. If the Federal Funds Rate is low and it is expected that they will be low over a 10 year period, then the expectation from the 10-year Treasury note is also lower. This is because the Federal Funds Rate impacts the short term borrowing rate between banks and even other short term bonds like the yield% of Treasury bills, which have a maturity of 1 year or less. Investors have a choice to make, either they can keep buying the 1-year Treasury bills over 10 years or they can buy a 10-year Treasury note. They know that there is less risk in the 1-year Treasury bills or other equivalent short term bonds as there is more certainty on the interest rates. So, they add some premium over these short term rates to set their expectations of yield% from a 10-year Treasury note.

- Fiscal Policy: This affects economic growth and inflation. It also determines how much debt the government will have as it will impact the Federal budget. A high deficit in the budget or expectation of a high deficit would mean more pressure on the US government to get debt to meet this deficit. To incentivize investors to give money to the US government, the yield% on the Treasury bills, notes and bonds will be higher.

- Economic growth: A high rate of economic growth or strong economy would tempt investors to buy equities rather than bonds due to expectations of higher returns. This would reduce the demand for bonds, like the 10-year Treasury notes, and the yield% on bonds would have to increase to attract investors. If the economy is weak, then the investors would look for safe investments like bonds, which will increase their demand and, as a result, reduce the yield% on them.

Wow, so it is the investors that determine the yield% on the 10-year Treasury note and even other Treasury securities. They are also responsible for deciding the secondary-mortgage spread. So, two out of three parts of the equation that sets the mortgage rates is controlled by the investors! I can see how capitalistic even the mortgage business is since everything is determined by market forces until the government has to step in times of crisis. This is such an amazing insight for me and overall I feel I have a better grasp on how the 30-year mortgage rates are set.

You are absolutely right, all the three parts of the mortgage rate equation are set by the expectations to make more money and hence it is a very capitalist approach. Where there are expectations to make money, there is a high probability of greed that makes people/institutions do unethical stuff. That is how the 2008 Financial Crisis happened, where greed got the better of people. It is therefore important that there are checks and balances so that these things are not repeated. I am glad you grasped the nature of the mortgage rates and will now track the right parameters to understand where they will go. Will talk to you soon! Happy holidays!

I surely know now what to look at! At least I know it is the 10-year Treasury note that needs to be tracked and not the Federal Funds rate to know where the 30 year mortgage rates are headed. It was great talking to you as always! Happy holidays!